While all aspects of a retirement plan need careful attention from plan sponsors, choosing the appropriate capital preservation option can be especially challenging. The options available to plans differ greatly and regulations surrounding money market options have become more complex since SEC reforms in 2016.

We like to help sponsors navigate these important choices. As experts in a variety of capital preservation strategies, we can help sponsors understand the differences in options.

Below we offer a video with Portfolio Manager Steven Horner that describes some of the key differences between the options, along with a performance comparison updated through the Covid-19 pandemic.

Putnam's Steven Horner, CFA, explains why stable value funds can pursue smoother performance

Comparing performance of capital preservation options — including during the Covid-19 pandemic

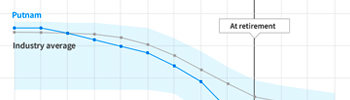

Over the long term, from 1987 through 2021, stable value funds have demonstrated a performance advantage over money market funds. This advantage is due to several factors, the most important being that stable value funds can invest in both short- and intermediate-maturity securities. In most market environments, intermediate-maturity securities offer higher expected returns than the universe of money-market-eligible securities. This key differentiator can be more or less advantageous, depending on the interest-rate environment.

As shown in the graph below, money market funds closed the performance gap in 2017 and 2018 as the Fed tightened policy. When the Fed cut rates in 2019 and dropped them to zero in 2020 as an emergency response to the Covid-19 pandemic, the advantage for stable value crediting rates over money market yields began to widen again.

Stable value funds vs. money market funds (rolling 5-year returns), 1987–2021

Source: Putnam.

What's more, the volatility profile of stable value funds has historically been lower than money market funds and much lower than intermediate-term bonds.

SEC reforms drove many plans to government money market funds

In 2016, the U.S. Securities and Exchange Commission completed reforms to the regulations that govern money market mutual funds. Under these new rules, both prime retail and institutional funds can impose liquidity fees and/or redemption gates under specific circumstances. Government money market funds, which invest 99.5% of portfolio assets in government securities, are exempt from these new regulations.

In the wake of the reforms, many investors chose to move assets to government money market funds from prime funds. DC plans, for example, found that the reforms made using prime money market funds nearly impossible because of the operational complexities required for plan recordkeepers. Many plan sponsors chose government money market funds instead and still hold those options.

We believe that DC plan sponsors might want to give stable value funds a deeper review. With a mix of smoother returns and outperformance in most market environments, these funds are often the better choice for a retirement plan.

Stable value funds offer an attractive combination of features

Learn more!

We describe our approach to capital preservation on our How We Invest page, and offer product information about Putnam Stable Value Fund.

You can also download FAQs and Three reasons to consider Putnam.

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.