Investors are concerned about decelerating economic growth and what this could mean for future equity returns. We researched this question to understand the historical relationship between an economic slowdown, earnings degradation, and any subsequent style or factor performance.

Methodology

We looked at the last 40 years and measured peak-to-trough real Gross Domestic Product (GDP) movement. We quantified the number of quarters of deceleration and the periods in which the slowdown occurred. See the data in Exhibit 1.

Periods of slowing economic growth

Exhibit 1: Peak to trough real GDP

Source: Federal Reserve Bank of St. Louis

We observe six periods of significant GDP deceleration since 1979. The median period of the economic deceleration was 14 quarters, with the minimum being four quarters and the maximum being 28 quarters. Importantly, not all these economic slowdowns resulted in a recession.

Source: Federal Reserve Bank of St. Louis, NBER. Shaded areas represent recession.

Earnings performance

We then quantified earnings degradation for the Russell 1000 Growth and the Russell 1000 Value indexes. See this data in Exhibit 2.

Exhibit 2: Earnings degradation

Source: Bloomberg, Putnam

The earnings data set is limited to 20 years. However, we believe the following observations still have merit. Earnings for the Russell 1000 value constituents declined by a median of -65.63%, while earnings for the Russell 1000 growth declined by a median of -9.01% during periods of GDP deceleration.

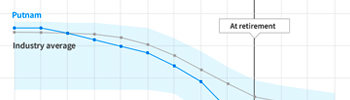

Style returns in periods of slowing economic growth

In periods of slowing economic activity, the Russell 1000 Growth Index outperforms the Russell 1000 Value Index. One explanation for this performance is that as the economy slows, fewer companies can grow earnings relative to periods of economic expansion where more companies can grow. Another reason may be that disruptive and innovative companies produce products or services that are not sensitive to changes in GDP. These companies may not rely on the tailwinds of a strong economy to grow their businesses.

Exhibit 3: Russell 1000 growth versus Russell 1000 value

Source: Bloomberg, Putnam

We observe that the Russell 1000 Growth Index generated a positive 9.39% annualized return during the six periods of economic deceleration back to 1979. The Russell 1000 Value Index generated a positive 4.15% annualized return during these six periods of slowing economic activity.

Factor returns in periods of slowing growth and earnings degradation

Investors may also consider what fundamental characteristics are rewarded during periods of economic slowdown and earnings degradation. We looked at the Fama and French factor model for insight. The Fama and French factor model is an asset pricing model initially developed in 1992 by Nobel Laureate Eugene Fama and Professor Kenneth French. In 2014, Fama and French adapted their original three-factor model to include two additional factors. One of these factors focused on “Profitability.” The Profitability factor suggests that companies that report more robust earnings have generated higher returns.

In this paper, we focused on the Profitability factor for large-cap equities. Fama and French calculate Profitability by taking a company’s earnings before tax divided by shareholder equity — essentially a pre-tax return on equity calculation. The higher the return on equity, the better, as it measures a company’s capital efficiency. The data universe includes all stocks listed on the New York Stock Exchange, the American Stock Exchange, and the NASDAQ. We calculated cumulative returns in the large-cap cohort on an equal-weighted basis, with terciles of Profitability as a measure of Quality in the large-cap space. Exhibit 4 illustrates the data.

Exhibit 4: Quality factor performance in periods of slowing economic growth and earnings degradation. Cumulative total return by tercile.

Source: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/index.html.

We observe that the first tercile of Quality generates more robust cumulative returns in-sample relative to the companies in the third tercile in five of the six periods of economic slowdown. This is significant and suggests that investors may want to focus on companies generating robust returns on equity during periods of worsening macroeconomic fundamentals. Said differently, investors may want to focus on profitability/quality during periods of economic stress.

Conclusion

In periods of economic deceleration, earnings have come under pressure. This holds true for the constituents in the Russell 1000 value and Russell 1000 growth universes. Historically, earnings degradation was significantly worse for Russell 1000 value constituents. The value components saw earnings decline by approximately 62% during periods of economic slowdown while the growth components saw earnings decline by approximately 9%. As a result, the Russell 1000 Growth Index outperformed the Russell 1000 Value Index during periods of economic deceleration. Specifically, the growth cohort had annualized returns of 9.39% relative to the value cohort annualized return of 4.15%.

During periods of economic deceleration, companies with stronger measures of Profitability, as defined by Fama and French, have outperformed companies with weaker measures of Profitability by a cumulative 21%, in-sample, and did so 86% of the time.

The views and opinions expressed are those of the authors, are subject to change with market conditions and are not meant as investment advice.

Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period; changes in GDP are an indicator of a nation’s overall economic health.

The Russell 1000® Growth Index is an unmanaged index of those companies in the large-cap Russell 1000 Index chosen for their growth orientation.

The Russell 1000® Value Index is an unmanaged index of those companies in the large-cap Russell 1000 Index chosen for their value orientation.

Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company.

For informational purposes only. Not an investment recommendation.

Putnam Retail Management

100 Federal Street

Boston, MA 02110

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.