Legislative and regulatory trends

The Defined Contribution (DC) industry continues to watch various packages of plan design reforms make their way through Congress. Rules that could affect auto-enrollment, IRA required minimum distributions (RMDs), catch-up contributions, and qualified charitable distributions, among others, hang in the balance.

Measures bundled in the SECURE 2.0 bill, also known as Portman-Cardin, could be addressed soon. The Senate has focused on other major legislation but could turn its attention to the bill early this fall or in this year’s lame-duck session after midterm elections. Any bill the Senate passes may be modified through the conference process with the House of Representatives. Nothing would be final until signed by the President.

On regulatory matters, new IRA rollover guidance is in full effect as of July 1, 2022. Retirement law under ERISA generally prohibits parties that are providing fiduciary investment advice to plan sponsors, plan participants, and IRA owners from receiving payments that create conflicts of interest, unless they comply with protective conditions in a prohibited transaction exemption. Since 1975, the DOL’s “five-part test” has allowed advisors to operate via a Prohibited Transaction Exemption (PTE). A new PTE 2020-02 is being enforced. PTE 2020-02 includes new disclosure rules, an investor-based best interest standard, new data collection and documentation requirements, and direction that reasons for rollover recommendations must be expressed in writing.1 These rules apply to all IRA rollover recommendations, not just rollovers from 401(k)s to IRAs.

Plan design trends

It is increasingly clear that, while plan design features such as auto-enrollment and escalation have served participants well, the industry has work to do when it comes to converting accumulated assets into reliable retirement income. The SECURE Act created a safe harbor provision for in-plan lifetime income provider selection. While in-plan guaranteed income products are available from recordkeepers, the industry is still working to wrap its arms around retirement income options and ongoing monitoring obligations.

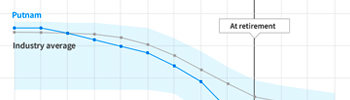

Similar development is happening around the notion of QDIA 2.0 (qualified default investment alternative). Modern data collection capabilities may make it feasible to offer QDIAs based on factors beyond a participant’s age, which has been the key data point for selecting target-date funds (TDFs). Features like customization (making plan-level adjustments to a TDF based on demographic or other factors) and personalization (making participant-level adjustments based on factors such as age, salary, retirement savings, and savings rate) are among the possibilities. Similar inputs may be used to create advisor-managed accounts, another form of QDIA 2.0. While questions remain about performance monitoring of customized and personalized approaches, the opportunities provided by harnessing the power of data are intriguing.

Financial woes on the rise

Source: Gallup.

DC investment trends

The search for investment economies of scale continues in the DC space. For 401(k) plans, this search continues to feed interest in collective investment trusts (CITs), which offer attractive fees.

As a point of reference, median fees in 2014 for large-cap equity mutual funds are reported to be 83 basis points, compared with 60 basis points for CITs.2 Modern CITs are available in most asset classes, are valued daily, and provide fact sheets and enhanced data reporting.3 With 401(k) litigation often focused on the use of a more expensive share class of a fund when a lower-cost alternative in a virtually identical strategy is available, the proliferation of CITs is likely to continue across plans of all sizes.

Watch for action on SECURE 2.0

As we look ahead to our next update, keep alert for news about Congress making progress on SECURE 2.0. Product and plan design trends will continue apace, but new legislation could accelerate many industry trends.

1 Ed McCarthy, "4 Tips to Avoid Rollover Problems Under New DOL Rule," ThinkAdvisor newsletter, July 5, 2022, https://www.thinkadvisor.com/2022/07/05/4-tips-to-avoid-rollover-problems-under-new-dol-rule/.

2 Coalition of Collective Investment Trusts, Collective Investment Trusts white paper, July 6, 2021, p. 9, https://www.ctfcoalition.com/portalresource/CollectiveInvestmentTrustsWhitePaper.pdf.

3 Ibid., p. 9.

331138

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.