When casting for plan sponsors, retirement plan advisors (RPAs) should be like great fly-fishers and start with the right questions.

Most accomplished fly-fishers believe that they have the experience, knowledge, and techniques to reel in the big ones. But these advantages don't impress fish. The key to fly-fishing is paying close attention to the fish. Specifically, this means asking what kind of recently hatched insects the fish are eating and deploying a fly that closely resembles these critters. Among anglers, this is known as "match the hatch."

A great RPA typically brings a hard drive's worth of ideas, strategies, and tools to their clients. In the interest of efficient client service and saving time for plan sponsors, they often get right to the point in meetings by coming with a set agenda. But this isn't "matching the hatch."

Great fishers, before they cast a line, pause to watch, listen, and read the river. Great RPAs should observe each plan sponsor in a similar way. This can be achieved through the simple strategy of asking thoughtful open-ended questions — and really listening to the responses from each 401(k) plan sponsor. To this end, we have developed five questions to organize your meetings.

Five questions to enhance plan reviews

How do you define plan success? What employee benefit enhancement or addition has your team discussed?

Plan advisors should take every opportunity to "check the pulse" of plan sponsors. Establishing long-term, big-picture goals is the best way to create context for multiple questions around enhanced benefit options and optimized plan design.

Defining success metrics can lead to measurement and monitoring that promotes shared vision around plan health.

Many well-intentioned plan advisors offer cookie-cutter plan reviews with similar agendas for each client. In today's world of customization and personalization, plan advisors can stand out by building reviews tailored to each plan, but only if they have a deep understanding of what is on the mind of their plan committees.

How happy are you with the corporate tax benefit provided by your retirement plan?

Given the pace of evolving regulation and industry practice, plan advisors should determine how CFOs and human resource officers feel about their 401(k) plan as a tool for tax efficiency at the company and participant level. Every dollar spent by a corporation on a retirement plan is a dollar-for-dollar deductible expense. Maximizing the tax benefit of retirement plans is an essential strategy. As companies change, regular plan design reviews may uncover design enhancement and tax-saving opportunities.

What labor force concern is top of mind for your HR team?

Having moved at breakneck speed through Covid policy implementation, the Great Resignation, and two waves of retirement legislation (the SECURE Acts of 2019 and 2022), only to now face labor shortages in many industries, HR leaders are under immense pressure. Checking in with these decision-makers using the question above can help a plan advisor uncover priorities that may or may not fall into the realm of traditional plan design.

What is the biggest frustration you have with your workplace retirement savings plan?

How happy are the employer and employees with their plan? How happy is the employer with you as their advisor? What benefits question would the sponsor like to cover? How much time and effort are needed to administer the plan?

Ask plan administrators: If you had to rank your plan on a scale of 1 to 10, how would you rank it? Does the plan committee agree? And what would it take to improve the ranking by one point?

Advisors can lose sight of the fact that the plan recordkeeper may be one of the best advocates for plan success. Are your plan sponsors happy with their recordkeeping relationship? Proactively uncovering recordkeeper challenges can save valuable time compared with reactively dealing with problems when they are out of control.

Advisors should coordinate the multiple service providers helping a retirement plan. Advisors can provide seamless service by seeing and directing the activity and interaction of service providers.

What should we talk about at our next plan review?

This simple question empowers plan committees and nudges them toward creative improvements, rather than just correcting problems. If it uncovers a here-and-now issue, advisors can address it. If a longer-term project is required, providing a look-ahead to the next meeting gives advisors and committee members time to prep and develop proactive ideas.

The world's best fly-fishers ply their craft with intimate knowledge of the river and the trout they pursue. Their techniques and strategies are built on deep understanding. This approach can be readily adapted to workplace savings plan reviews. Retirement plan advisors should "match the hatch" by uncovering what is on their clients' minds.

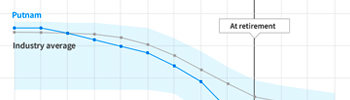

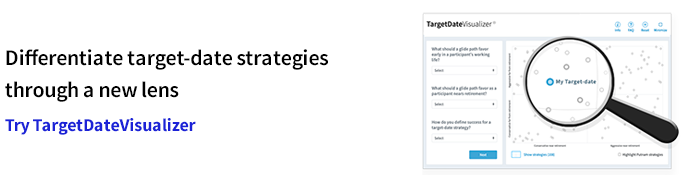

Whether your open-ended-question-based reviews uncover opportunities for a core menu/model review, plan design optimization, or target-date selection, Putnam DCIO can help. Our VisualizerSuite of industry-leading digital tools is designed to make your workflow efficient and effective.

Incorporate our open-ended questions to create bespoke plan reviews and use our VisualizerSuite of digital tools to create customized solutions for each plan.

Use TargetDateVisualizer as your TDF evaluation tool today.

334481

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.