- The municipal bond market recorded its fourth-best year of inflows.

- The prospect for higher taxes for corporations and high earners may play a role in demand.

- Reduced supply of tax-exempt munis led to higher valuations for some sectors.

Demand for municipal bonds continues to be robust in 2021.

Like all asset classes, the muni market faced challenges from declining tax revenues caused by the Covid-19 pandemic in 2020. Still, by December, munis recorded the fourth-strongest year on record of mutual fund inflows.

Technicals are the story

In March and April, investors pulled $48 billion from the muni market in a five-week period. The selling caused a dramatic increase in muni yields. The environment improved with federal fiscal stimulus and support from Federal Reserve lending facilities. The muni market came back rapidly, and ended the year with strong inflows, taking in a net $40 billion.

The Fed’s September 2020 announcement that it expected to hold short-term interest rates near zero until the end of 2023 also fueled interest. With yields on certificates of deposits and U.S. Treasurys near zero, investors sought out other alternatives. Although municipal bond yields were lower as well, their after-tax income advantage remained compelling. In other cases, investors perceived tax-free bonds as an attractive alternative to the volatile equity market. We also believe the prospect for higher taxes for both corporations as well as higher-income individuals played a role. These factors contributed to a strong demand environment that helped push bond prices higher. As interest rates have moved modestly higher in February, we continue to closely monitor the markets and quickly reposition the portfolio to take advantage of changing trends.

Post-election positive momentum

The supply of new municipal bonds issued after the November U.S. elections fell below last year’s totals, amplifying the strong technical backdrop.

The demand story continues in 2021. In recent weeks, municipal bond mutual funds took in $6 billion in one week — the largest weekly inflow on record.

On the supply side, the market experienced a bifurcation. Tax-exempt issuance slipped 3%, while taxable municipal bond issuance doubled from the prior year. The main catalyst was a provision of the Tax Cuts and Jobs Act of 2017 that eliminated advanced refundings (refinancings). Municipal issuers used taxable muni bonds to refinance older, higher coupon tax-exempt debt.

Banks and insurance companies have lately led the way among institutional buyers. In fact, banks purchased about $60 billion in municipal bonds in the fourth quarter, marking the largest total since 2003. Retail demand has also been strong.

Improving fundamentals

Credit fundamentals are stabilizing. The pandemic had a significant impact on state and local revenues. In October, Brookings projected a $317 billion budget gap in state and local budgets over the next two fiscal years. In 2020, Moody’s estimated the decline in state and local tax revenue could leave a deficit between $200 billion and $400 billion.

Some state revenues fell more than others. States in popular leisure destinations, like Nevada and Florida, felt the economic pain as mobility restrictions were implemented. Overall, states with income taxes have navigated the pandemic better than states that rely more on sales taxes, for example. The revenue declines were not as steep as projected. Some states reported beating post-pandemic revenue expectations. For example, early in FY21, California tax revenues were $8 billion higher than expected and Massachusetts saw an increase of 4%, while New York and New Jersey saw their FY 2021 revenues lagging a modest 2% to 3%.

The CARES Act provided significant support for state and local governments, colleges and universities, and healthcare organizations. The Fed’s Municipal Loan Facility, which ended in December, was unprecedented in the muni market and gave investors confidence that municipal borrowers could access liquidity if needed.

More support is anticipated. The latest pandemic relief bill in debate — The American Rescue Plan — would provide $350 billion for state and local governments. The proposed amount represents nearly 15% of state budgets. Even if the amount in the final legislation is lower, additional revenues will help states’ and local governments’ fiscal profiles.

Defaults remain low. In 2020, the 80 defaults were the highest total since 2013. Consider, however, that the 10-year average is 79 (Source: Municipal Market Advisors). Although defaults have risen, defaults remain a very small percentage of the overall Municipal bond market — less than ¼ of 1% overall. Downgrades outpaced upgrades, but we do not believe that is a problematic trend and it highlights the advantage of Putnam’s deep municipal bond credit research team.

Muni fundamentals withstood a lot of volatility in 2020. We think we are coming out on the other side. With the American Rescue Plan, as well as easing of mobility restrictions, our economists believe U.S. economic growth will be robust in 2021.

Valuations high in some segments

As more investors pursued fewer municipal bonds, lower yields and spreads resulted in higher valuations for some high-quality tiers of the market. This created expanding opportunities in the lower-rated tiers. The muni-treasury ratio (comparison between current rate of municipal bonds and U.S. Treasury bonds) highlights that municipal bonds remain somewhat expensive versus U.S. Treasury bonds. At Putnam, we believe the best place for income and return are in the lower-rated tiers of the investment-grade market, such as BBB credits, and in certain high-yield bonds. Our experienced team of municipal portfolio managers, credit research analysts, and traders work together to construct portfolios to deliver competitive tax-exempt income along with the possibility of future price appreciation.

Overall, we believe the municipal bond asset class remains sound and represents an important choice for investors to receive attractive tax-exempt income in a high-quality, low-default asset class.

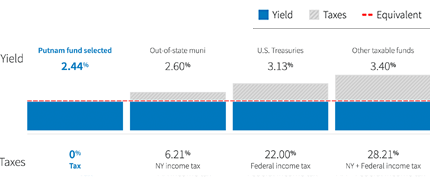

Evaluate yields on a tax-equivalent basis

Compare municipal funds on equal footing with taxable bond funds.

325153

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.