- There is no “one size fits all” narrative around the effects of the COVID-19 crisis on the financials sector. Some industries will be hurt more than others.

- Most of the largest financial institutions are reserving enormous sums in anticipation of future loan losses.

- Today, U.S. banks are part of the solution to the crisis, rather than the cause, as they were in 2008.

The financials sector has been among the hardest hit from the COVID-19-induced equity market selloff, underperforming the Russell 1000 Value Index considerably in the first quarter. This pain has been particularly acute as lower interest rates pressure net interest margins — the difference between interest earned and interest paid on loans and deposits. Also, the deepening economic malaise has raised concern over credit from consumers and corporations alike. The financials sector — and banks in particular— tends to have very high sensitivity to the macro economy.

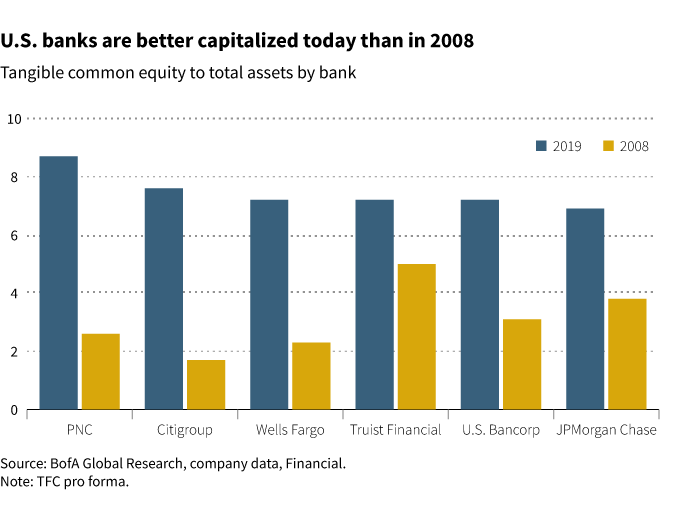

U.S. banks are well capitalized

It is important to note that the U.S. financials sector was in considerably better shape coming into this crisis than it was for the 2008/09 global financial crisis. With that crisis, irresponsible lending and leverage exposed insufficient capital levels and caused systemic failures. Today, U.S. banks are very well capitalized as a result of much stricter regulation, and they are part of the solution to today’s crisis, rather than the cause, as they were in 2008. There is no concern in the market around capital levels, and the largest U.S. banks are maintaining their dividends, unlike many of their global peers. Deposits to the largest four U.S. banks have increased by over half a trillion dollars since the onset of the pandemic crisis. These banks are playing an essential role in transmitting Federal Reserve and Treasury policy into the markets.

There is no concern in the market around capital levels, and the largest U.S. banks are maintaining their dividends, unlike many of their global peers.

There is certainly increasing risk around credit, and we have seen most of the largest financial institutions reserving enormous sums in anticipation of future loan losses. The largest four institutions put aside almost $25 billion in the first quarter. This has materially lowered earnings, but has also anticipated terribly adverse economic scenarios. These reserves are likely to continue to build in the coming quarters, but visibility remains very low. Policy actions have been historic in both their size and the speed at which they have come to market. They represent a metaphorical “bridge loan” to the U.S. economy, both at the corporate and the individual level. Importantly, in setting aside reserves, none of the major banks have accounted for potential stimulus, either fiscal or monetary, to lighten the losses they incur through the crisis.

In setting aside reserves, none of the major banks have accounted for potential stimulus to lighten the losses they incur through the crisis.

Some industries will be hurt more than others

The impact of the crisis will have varying effects on industries within the financials sector. For example, credit card businesses have set aside the most in reserves. This is because the uncollateralized nature of this type of lending makes it considerably more vulnerable to future losses than, for example, a loan to a high-quality corporation with a strong balance sheet. On the other hand, many of the market-related businesses, such as trading and investment banking, have seen considerable increases in momentum on the back of the crisis. In short, there is no “one size fits all” narrative around the effects of the COVID-19 crisis on the financials sector.

In the final analysis, financials have higher sensitivity to market and macroeconomic declines, but they will also have higher sensitivity to a return-to-normal scenario.

The depth and duration of the recession and eventual shape of the recovery will matter most to the sector. The high level of uncertainty around the pandemic crisis is precisely why we have seen the U.S. financials sector underperform the broader market. While many of the largest banks remain profitable and well reserved, we are maintaining underweight exposure to the broader financials sector in our portfolio, relative to the benchmark. In the final analysis, financials have higher sensitivity to market and macroeconomic declines, but they will also have higher sensitivity to a return-to-normal scenario. We believe banks are trading at very reasonable levels relative to their tangible book value.

Learn more about Putnam Equity Income Fund.

Putnam Equity Income Fund

Top 10 holdings as of 3/31/20

Microsoft, 4.33%

Walmart, 3.23%

JPMorgan Chase, 3.06%

Bank of America Corp, 2.93%

Citigroup, 2.55%

Johnson & Johnson, 2.40%

Northrop Grumman, 2.30%

American Tower, 2.00%

Cigna, 1.94%

Merck, 1.82%

Top 10 holdings, percent of portfolio: 26.56%

321642

Consider these risks before investing: Value stocks may fail to rebound, and the market may not favor value-style investing. Income provided by the fund may be reduced by changes in the dividend policies of, and the capital resources available at, the companies in which the fund invests. The value of investments in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general economic, political, or financial market conditions; investor sentiment and market perceptions; government actions; geopolitical events or changes; and factors related to a specific issuer, geography, industry, or sector. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio holdings. You can lose money by investing in the fund.

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.

![ESG Materiality: A North Star for multi-asset investors [2023]](/static/img/blogs/perspectives/334257_1200x627.jpg)