When the tax landscape is uncertain, flexibility can be a key part of any planning strategy. Sometimes tax policy changes can undermine well-intentioned financial plans.

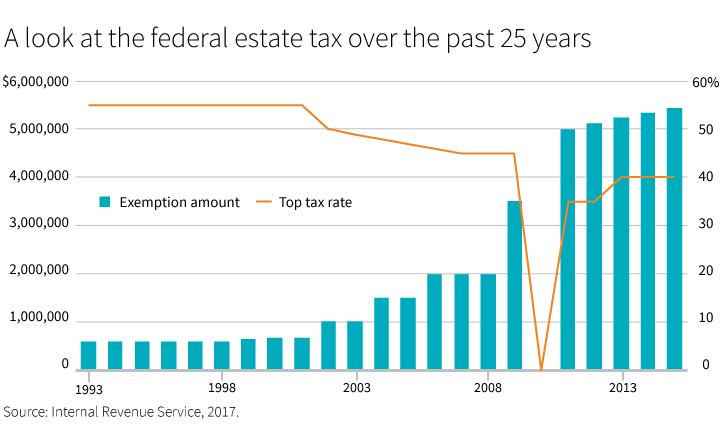

Estate planning is no exception. Changing tax laws may impact important figures such as the federal tax exemption amount and the marginal federal tax rate on estates. A look at recent history illustrates how dramatically changes can unfold. Due to an omission in the tax law, there was no federal estate tax in 2010 — the first time in nearly 100 years. The following year, the tax was reinstated. After fluctuating for several years, federal estate and gift tax exemption levels were made permanent by the American Taxpayer Relief Act in 2013. The law also included an adjustment for inflation.

Today, after a few years of clarity, the future of the estate and gift tax is shifting again as Congress considers comprehensive tax reform. Among the proposals on the table is a repeal of the federal estate tax, and prospects for the federal gift tax are unclear.

Flexibility is key

While Congress is tackling the tax code, some investors may prefer to hold off on certain estate planning strategies until tax reform is resolved. But investors may risk losing advantages from some estate planning strategies, for example while interest rates are still relatively low.

In this environment, investors may be reluctant to establish a trust — especially an irrevocable trust. Once an irrevocable trust is created, investors are limited in making major changes to the terms.

But even when a trust is irrevocable, investors may have some flexibility if the state where the trust is created has a provision allowing for the decanting of trusts. Decanting generally involves distributing assets from an irrevocable trust to a new trust with different terms. This strategy may be helpful if the tax environment changes and it causes unintended consequences for an existing trust.

Currently, about 25 states allow trustees more flexibility in decanting existing irrevocable trusts. Additionally, more states are considering decanting rules. Investors may want to meet with a financial advisor and estate planning professional about using decanting laws for their advantage. It is also important to work with a qualified estate planning attorney as the laws and requirements can vary among states.

For more detail, this listing provides more information about state laws.

306210

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.