- Parents sending children to college for the first time may need guidance on paying for college

- Planning strategies may help families optimize their college savings

- Distributing 529 college savings plan assets may have an impact on financial aid and taxes

It’s July and the tuition bill has arrived for college. Are families prepared to access their college savings?

As students focus on registering for classes and picking out dorm room essentials, many parents sending children to college for the first time face a couple of challenges: How to implement financial planning advice on paying for college, and how to maximize their 529 plan savings, in particular.

529 plan considerations

Nearly one third of families use a 529 college savings plan to save for their child’s education. There are tax advantages unique to a 529 account, including tax-free earnings as long as distributions are made for qualified higher education expenses. There are also many rules about distributions that families need to know and may want to review with a financial advisor in advance. Some of these decisions are important for getting the optimal results from a college savings plan.

Rules governing the timing of 529 distributions

- A distribution can be taken at any time, and is tax-free as long as an equal or greater amount of qualifying expenses are paid during the same year. In other words, the use of the distribution proceeds does not have to be traceable to the actual payment of college expenses. But the amount must still be reflected as a distribution during the calendar year.

- If you withdraw money from your 529 this calendar year and use the money for next year (spanning two tax years), you risk penalties on at least portions of the distribution. Some college bills arrive in December, but payments may not be due until January or the second semester in the spring. There is no exact guidance from the Internal Revenue Service (IRS) on how to handle this situation, so it is important to keep track of distributions and payments. For those with tuition bills due January 1 (for second semester expenses), some families may want to consider tapping other accounts in late December to make the January deadline and then distributing from the 529 early in the next calendar year to “pay themselves back.” In this way, the 529 distribution will match up with the second-semester expenses within the same calendar year.

How tapping into a 529 affects taxes

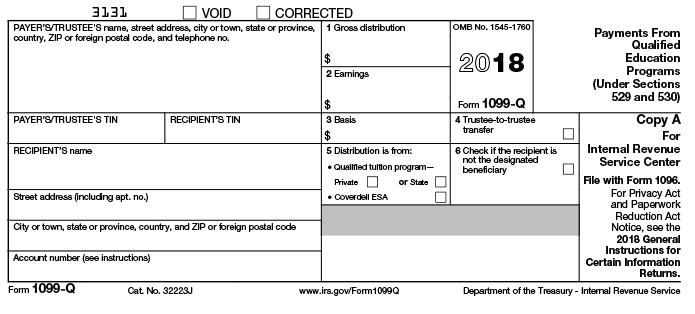

If you take a distribution from a 529 account, you’ll receive a Form 1099-Q, which must be reported on a federal income tax return. This form is used to detail qualified higher education expenses and total distributions. The 529 distribution is considered a pro rata portion of contributions and earnings. If distributions exceed the amount used for qualified expenses, the excess is considered a non-qualified distribution, so it is important to keep track of this information. If 529 funds are being used for room and board expenses (on- or off-campus), keeping those receipts will be essential.

You can choose to send the distribution to the beneficiary, to the school the beneficiary is attending, or to yourself, the account owner. With the first two options, the beneficiary will later receive a 1099-Q for that tax year. If any part of the withdrawal is used for non-qualified expenses, the earnings portion will appear on the beneficiary's income tax return where it may be subject to a lower tax rate than yours. If you select the school, it may help avoid the timing mismatch of the calendar year.

Coordinating federal tax benefits to help pay for college

There are several tax credits available to help families with higher education costs. Parents also need to consider scholarships and try to plan ahead using the IRS Form 970.

Lifetime learning, American Opportunity Tax Credit

- The maximum $2,500 American Opportunity Tax Credit consumes $4,000 of qualified expenses. In most cases, this will result in a $4,000 reduction to the 529 expenses.

- To be safe, limit your 529 plan withdrawals to your beneficiary’s total qualified higher education expenses, less $4,000. If you are not eligible for the American Opportunity Tax Credit, but plan on claiming the Lifetime Learning Credit, the adjustment can be as much as $10,000.

- “Double-dipping” is not permitted when using a 529 plan and claiming education tax credits. If you, or your beneficiary, claim either the American Opportunity Tax Credit or the Lifetime Learning Credit on your federal income tax return, you must adjust total qualified expenses for purposes of determining the tax treatment of your 529 plan distributions.

Dealing with multiple 529 accounts

Different accounts are going to experience different growth rates. By first tapping the account with the higher earnings rate once your child gets to college, you are locking in maximum tax savings. If your child graduates when you still have money in 529 plans, the tax cost associated with non-qualified distributions is minimized because the lowest-growth account is left for last.

If family members have additional accounts, talk with them to coordinate a strategy about when to tap into these funds. For example, if financial aid is in the picture, a distribution from a grandparent-owned 529 account may be considered income to the child on the next financial aid application, which could significantly affect the award.

If parents have more than one child in college at the same time, it’s important to avoid causing a taxable event for any of them. If one has higher tuition, parents can move money between accounts for better balance. At the same time, they cannot take all the money from one child’s account to pay for both children.

Additional options

Families may also want to explore whether the college offers an installment plan so they can break up the tuition balance into monthly payments. These plans typically have an enrollment fee that can average $30 to $100. Often this fee is lower than fees for a student loan.

If there is money left over in the 529 account once all of a child’s undergraduate expenses are paid, it may be used to fund graduate school or transferred to another family member through a beneficiary change.

A drawdown strategy can optimize results

The process of saving for college can be a complicated one and savers need to pay attention to account limitations in order to avoid tax liabilities. To optimize college savings, it’s just as important to develop an efficient drawdown strategy as it is to save. Seeking advice from a financial professional may contribute to achieving your goals. For more information about college savings and developing a drawdown strategy, read Putnam's investor education piece, "Strategies to make the most of college savings."

312310

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.