With sweeping retirement legislation garnering massive support in Congress, concerns about the future of the stretch IRA have resurfaced.

A stretch IRA strategy allows non-spouse beneficiaries to “stretch” out required minimum distributions (RMD) based on their remaining life expectancy after inheriting the IRA. The strategy extends the life of the IRA by continued, tax-deferred growth even after the death of the owner. The younger the beneficiary inheriting the IRA, the lower the required minimum distribution, which means more assets remain in the account sheltered from taxes.

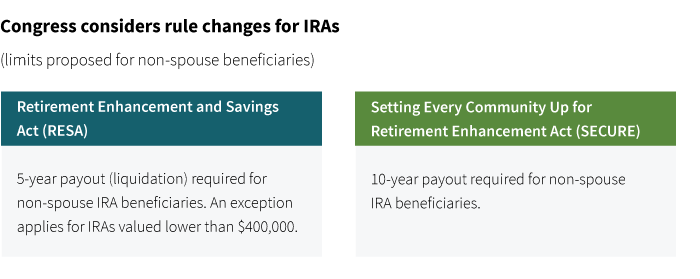

For several years, lawmakers have attempted to pass legislation that would end this strategy, putting the beneficiary at risk for a higher tax bill.

With the recent passage of the SECURE Act by the House, policy makers are getting closer to that goal.

How a stretch IRA works

After an IRA owner dies, federal tax law requires non-spouse beneficiaries to withdraw a specific minimum amount each year. The beneficiary can maximize the life of the IRA and defer taxes on those assets for as long as possible. To do this, beneficiaries will want to withdraw as little as possible, preferably the required minimum each year.

Consider this example:

- John owns an IRA worth $250,000 and is 80 years old. His RMD is $13,368 this year (based on the IRS uniform life expectancy table) [$250,000 divided by LE factor of 18.7 based on table = $13,368 RMD]

- John dies and his granddaughter Karen (age 22) is the sole beneficiary

- RMDs going forward for Karen will be lower since her life expectancy is higher

- Based on her age at 22, with an inherited IRA worth $250,000, the RMD would be only $4,091 (based on IRS single life expectancy table) [$250,000 divided by LE factor of 61.1 based on the single life table = $4,091

For more detail, read Putnam’s investor education article, “Stretch an IRA over generations.”

Lawmakers eye changes to stretch IRA

The stretch IRA has been under the scrutiny of lawmakers for several years. For example, legislation proposed in 2014 would have significantly scaled back the ability for non-spouse beneficiaries to stretch their RMDs. In most cases, these IRAs would have to be liquidated in a five-year period following the owner’s death.

Current legislative proposals on Capitol Hill provide for a phaseout or limited use of the stretch IRA strategy.

Consequently, without the ability to stretch distributions over many years, the beneficiary will see a larger tax bill in some cases.

Planning considerations if the stretch option goes away

- Non-spouse beneficiaries inheriting IRAs may need to carefully plan for the tax bill on distributions out of the IRA. If the beneficiary is required to liquidate the IRA in a shorter time frame, it may move them into a much higher tax bracket. Non-spouse beneficiaries will want to time the liquidation of the IRA in a year, or years, where their overall income may be lower. Or they may want to make larger charitable deductions in a year when the IRA funds must be withdrawn in order to offset the increased income.

- The lack of the stretch option makes an IRA a less attractive asset to pass on to the next generation. IRA owners may want to consider spending more IRA assets while living or giving to charities tax free through the qualified charitable distribution (QCD) option.

- Rather than rely on IRAs for intergenerational wealth transfer, investors may want to consider other tax-advantaged options. If structured properly, whole life insurance can provide an income and estate-tax free legacy to the next generation.

- For clients with philanthropic objectives, naming a charitable remainder trust (CRT) as an IRA beneficiary may be a means of providing a lifetime income stream to heirs in a tax-advantaged manner.

- The demise of the stretch option may make Roth IRAs more attractive. Although they also would be subject to the new payout rules as well, beneficiaries would not have to plan for potential “bracket creep” that would apply to taxable IRA distributions.

- IRA owners may want to reconsider beneficiary designations on IRAs. For example, it may make more sense from a tax perspective to designate beneficiaries who are in lower marginal income tax brackets. Other assets, like appreciated stock held outside of retirement accounts, may be more appropriate to leave to beneficiaries in higher tax brackets considering that these assets will generally benefit from a step-up in cost basis at death.

Revisit estate plan

The potential loss of the stretch IRA option has many implications for investors, particularly in the areas of tax efficiency and estate planning. Investors may want to consult with a financial advisor to review current tax and estate plans and determine whether updates are needed to meet their goals.

317346

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.