The recent proposal from the Biden administration — The American Jobs Plan — calls for broad spending across multiple areas, including traditional infrastructure, clean energy initiatives, and other areas such as health-care funding for the “care economy.”

With a projected cost of over $2 trillion, the proposal also includes tax increases for corporations (“Made in America Tax Plan”), designed to partially offset the cost. Central to these proposals is an increase in the corporate tax rate from its current level of 21% to 28%.

If approved, the tax increase could impact how certain business owners structure their companies.

Increase in corporate rate may cause business owners to act

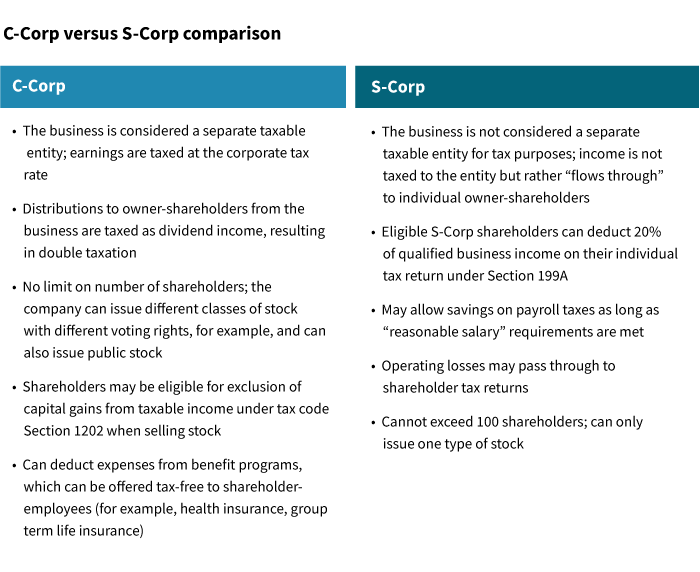

- Some small business owners currently operating as C-Corporations may be prompted to re-think those structures if the corporate tax rate increases

- Specifically, business owners may consider whether it makes sense to continue being taxed at the corporate rate, or transition to an S-Corporation and be taxed as a flow-through entity at individual tax brackets

Making the transition from C-Corp to S-Corp

- Currently the difference in the maximum tax rate (not including taxation of distributions from C-Corps) between C-Corps (21%) and S-Corps (roughly 29%, assuming top individual tax rate of 37% with a 20% deduction for qualified business income (QBI) ) is around 8%

- If the corporate tax rate is increased to 28%, then there is no meaningful difference. Because of this, and the double taxation issue, some C-Corp business owners may consider restructuring their business to an S-Corp. Of course, there could be proposals from Congress to scale back the 20% QBI deduction applying to pass-through business owners like S-Corps. This would increase taxes on some S-Corp businesses and impact a decision to transition from C-Corp to S-Corp

- The Internal Revenue Service outlines the filing requirements for making a status change

Consult with an expert

Because of the complexities, the move from a C-Corp to an S-Corp should be carefully considered with the expertise of a qualified tax and legal professional. For example, there may be adverse tax issues associated with converting from a C-Corp to an S-Corp, such as unused net operating loss (NOL) carryforwards or built-in gains tax, which may be assessed to S-Corps that were formerly C-Corps.

325927

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.