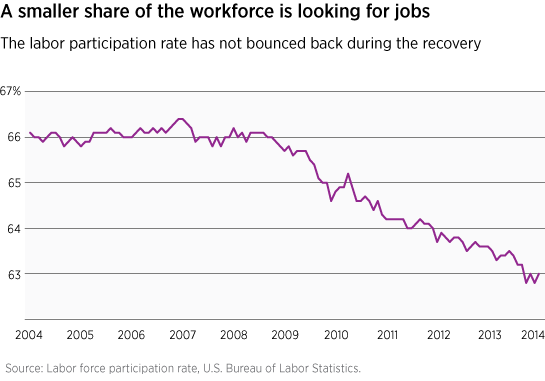

Unemployment continues to drop, but not because a lot of new jobs are being created, as many would hope. Instead, the unemployment rate is dropping primarily due to a declining labor participation rate.

This remains a cause for concern for us because of what it could mean for inflation.

The Fed, under Chairman Ben Bernanke, believed that an easy money policy — which tapering will not eliminate this year, but only gradually reduce — would generate enough cyclical dynamism to counteract any negative effects of the prolonged downturn. While the economy has remained in recovery, GDP growth has been less than dynamic.

Furthermore, the Fed continues to believe that the non-accelerating inflation rate of unemployment (NAIRU) — the rate to which unemployment can fall without triggering wage inflation — is around 5.6%. However, our research suggests, and some institutions share the opinion, that the NAIRU may be significantly higher than this, primarily because of various structural problems hampering the labor participation rate.

Generally speaking, investors believe wage inflation could become a problem sooner than expected.

As the unemployment rate moves downward, if wage inflation develops earlier than the Fed is anticipating, we could see the central bank reduce its stimulus efforts much earlier than the markets are currently forecasting.

We do not see this eventuality coming to pass during this winter, but it could be a development that raises significant concerns for the Fed and the markets later in 2014.

Read Putnam's Fixed Income Outlook.

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.