Since 2009, we have warned that the Barclays Aggregate indexes (the U.S. Agg and the Global Agg), which serve as benchmarks for trillions of dollars of investors’ money invested in mutual funds and other vehicles, represent a diminished set of opportunities for fixed-income investors.

Our view continues to be that more attractive forms of risk can be found outside these indexes.

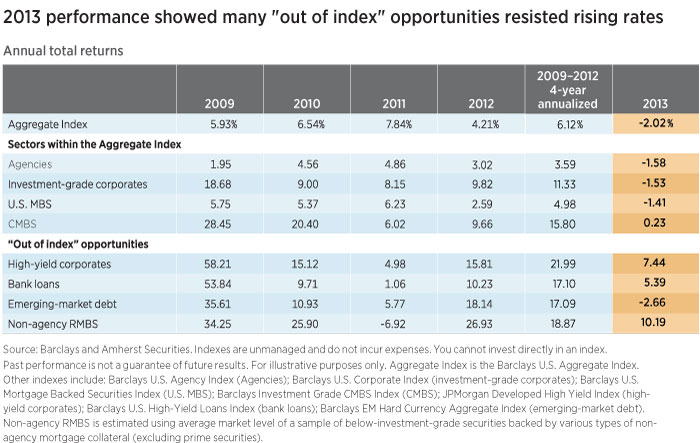

Performance history supports our view

While Agg-benchmarked products and generally longer-duration portfolios avoided poor results in the first four years after the financial crisis, the true risk of the Agg’s composition began to emerge in 2013. With interest rates coming unmoored from their historic lows, our thesis on the Agg — especially our focus on its vulnerability to interest-rate risk — began to prove itself out, particularly after the U.S. Federal Reserve began to discuss “tapering” its bond-purchase program.

Performance records compared: in and out of the index

In the years since the financial crisis, spreads in various fixed-income sectors, both within the index and outside it, have tightened dramatically from their historically wide levels, retracing much of the widening that occurred in the 2008–2009 period. Of course, spread compression during this period led to historically large returns for virtually all fixed-income asset types.

But as the table above shows, 2013 marked a watershed moment for index versus non-index sectors in fixed income. With the exception of emerging-market bonds — which, during the second half of 2013, experienced a strong downdraft due to foreign investor outflows amplified by currency weakening — out-of-index opportunities soared while the Agg and many of its components suffered. In 2013, the Barclays U.S. Aggregate Index delivered a return of -2.02%, marking the first calendar year that the index was in negative territory since 1994.

Index-related risk may be an emerging trend

We fear this could become a recurring theme over the next few years if interest rates should embark on a sustained rise, as we expect them to. This could be the case until we return to a more “normalized” world in which investors are compensated with higher yields given the level of interest-rate risk (duration) they are taking.

290764

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.