Today, the United States' economy is growing while Europe's is essentially flat. And the difference between these two trajectories may come down to policy paths taken or not taken.

While governments on both sides of the Atlantic have reduced their deficits over the past five-plus years, they have taken substantially different approaches to achieving this important goal. In Europe, policymakers have leaned quite a bit more than their U.S. counterparts on reducing spending. This has put downward pressure on Europe’s GDP growth. In the United States, there has been more focus on so-called “quantitative easing” programs, and we have continued to see rebounding GDP.

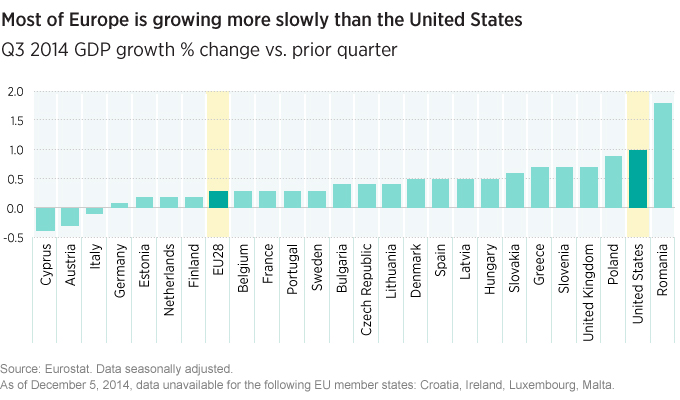

Europe playing catch-up to the United States

In terms of monetary policy, the United States thus appears to be a couple of years ahead of Europe. As early as 2008, U.S. policymakers initiated a fairly aggressive monetary stimulus program and quantitative easing, involving trillions of dollars of government bond purchases and other direct market interventions.

Now, shortly after the United States finished winding up its bond-buying activities, Europe has made its first major foray into its version of quantitative easing. While this so far has included different types of asset purchases, no commitment to buy European sovereign debt has as yet been made. Hopefully for Europe, growth — and inflation levels — will accelerate over the next 6 to 12 months.

Differences within Europe

In Europe, it should be noted, not all countries have approached reform in the same way, and there are important intra-regional differences that we have observed and continue to monitor. In one regard, the degree of flexibility in labor laws varies by country, which has an impact on unit-labor costs across the eurozone.

Spain, for example, moved aggressively with respect to its unit-labor costs in order to become more competitive on the global stage. Consequently, Spanish exporters have improved their conditions more than have exporters in some of the other peripheral European countries.

Italy and France, by contrast, have struggled because of the relative inflexibility of their labor laws and relative fixed unit-labor costs.

292347

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.