- Demand for U.S. government debt in a low-yield world has helped keep a lid on interest rates

- Rate risks still loom, in part because policy measures holding down rates could change

- We believe an unconstrained approach remains warranted to complement rate-driven strategies

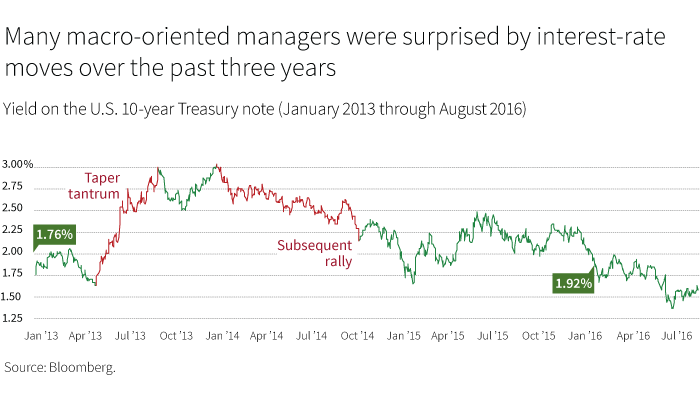

Since the taper tantrum in 2013, when the market reacted negatively to comments by Fed officials about planning to taper off asset purchases, the interest-rate and inflation environment has been generally benign. Strategies aligned with the interest-rate risk embedded in common benchmarks such as the Bloomberg Barclays Global Aggregate Bond Index and the Bloomberg Barclays U.S. Aggregate Bond Index have performed well, outperforming most unconstrained strategies.

However, while rates have ratcheted downward, upward movements in the 10-year Treasury yield suggest that the market has remained on watch for a rapid shift in the interest-rate outlook. Investors, aware that central bank policies have contributed to moving rates to their current levels, recognize that both policies and rates could move in a new direction with little warning.

Flexibility and diversification help prepare for the unexpected

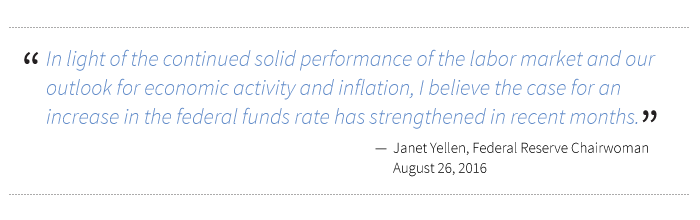

At a time of global policy divergence, we believe it makes sense to be prepared for rapid shifts in market expectations. The Fed has reacted to emerging data over the past year in ways that kept a lid on rates, but this data-dependency means that its intentions could change when data trends change. For example, in the immediate aftermath of the Brexit referendum, it appeared another rate hike in 2016 was off the table. Yet, by early August, a Wall Street Journal survey of economists pointed to December as the most likely time for the next rate hike.

Meanwhile, in Europe and Japan, where central banks are experimenting with negative-interest-rate policies, it is questionable whether they are obtaining the results that they had hoped for. GDP growth remains extremely sluggish, and, in the case of Japan, a stronger yen hurts exporting companies. While neither the European Central Bank nor the Bank of Japan is yet commenting on changing these policies, headwinds exist. Questions surrounding the supply of bonds that the ECB and the BoJ can buy, for example, may pose an obstacle to these policies.

Uncertainty over policy may make it attractive to have flexibility in an interest-rate strategy, combined with other types of investment flexibility that come with an unconstrained approach. Investing beyond the constraints of an index allows an unconstrained approach to pursue opportunities in corporate and mortgage credit sectors and in emerging markets. In all of these areas, fundamental credit research can be valuable for identifying sources of potential return that can supplement strategies that depend on falling rates.

302965

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.