- Saving for retirement can be made simpler with target-date funds

- Target-date funds are built with a glide path feature that systematically manages diversification

- When comparing glide paths, risks near the start of retirement merit particular attention

When it comes to saving for retirement, a target-date fund is sometimes labeled as a one-size-fits-all solution. But a closer look reveals that built inside these funds is a careful management approach to multiple investment risks — all with the purpose of keeping savers on path toward a secure retirement.

Looking under the hood

Financial professionals approach retirement as an investment challenge that involves accumulating a certain level of savings by a future date — the target date. It requires first helping to maximize savings growth and then, over time, increasing focus on preservation. The time frame during which this balance must be adjusted is commonly referred to as the “glide path.”

Automatic allocation adjustments

The glide path guides how asset allocations shift over time, as savers progress toward their retirement date. Everyone saving for retirement is on a glide path and hoping for a safe landing, but will nonetheless experience the same ups and downs of stock and bond markets between today and that future date. While it is unknown exactly when markets will be volatile, the glide path takes this into account by reducing risk when it is most important — near and in retirement.

Different managers have different approaches

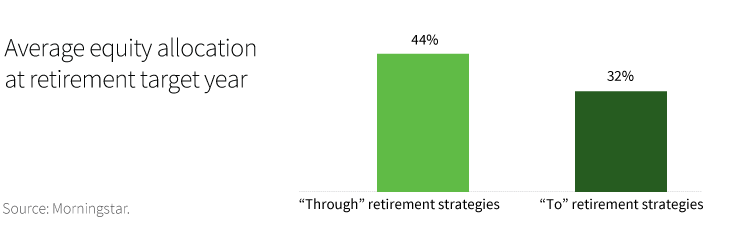

When and how much allocations adjust will vary based on the approach taken by the fund manager. Glide paths can be classified as “through” or “to” strategies. “Through” glide paths are designed for the saver’s working years and retirement years. The glide path continues to adjust after the investor’s retirement date.

A “to” retirement strategy means that asset allocations change until the retirement date. The allocation after the retirement date remains the same.

Opinions differ about whether the “to” or “through” approach is better, but for most savers, the important consideration is to be aware of the different characteristics of these approaches. A “through” strategy typically owns more equities at retirement and may be more volatile. A “to” strategy is likely to have a lower equity allocation at retirement and may be less volatile.

Simple by design

Target-date funds are an important innovation and provide a thoughtful glide path that automatically diversifies retirement savings to reduce risk near retirement. For savers, they offer greater simplicity than building and maintaining a portfolio of many investments over many years. Nevertheless, it remains important to understand some of their design details in order to maximize their potential.

The principal value of the funds are not guaranteed at any time, including at the target date.

308744

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.