- One third of employers offer help to employees paying student loans (Source: EBRI)

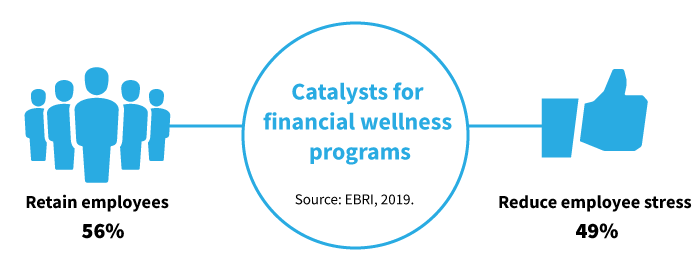

- Financial wellness programs are a top employee retention tool, employers believe

- Senators introduced a proposal to permit workers to pay college debt by tapping 401(k)s

Starting a career with a mountain of college debt is a big concern among new graduates deciding how to budget their income. This problem is widespread. Across the economy, student debt has grown to more than $1.5 trillion. While the issue may be making more headlines today, employers have been working to resolve this challenge for many years.

Employers are paying attention

College debt assistance is becoming a more common part of the benefits discussion. A growing number of companies are introducing programs to help employees manage student debt. These programs range from help with debt consolidation or refinancing to loan repayment subsidies paid by the employer.

A recent survey by the Employee Benefits Research Institute found:

- One third (32.4%) of employers offer, or plan to offer, a student loan debt program

- 40% of employers have “high” concern about employees’ financial wellbeing

- Employee retention was the number one reason cited by companies that offer student loan debt programs

Congress considers action

Workers may see even more programs emerge if Congress advances a proposal to allow companies to make a “matching” contribution to a 401(k) plan as long as the worker is making a specified minimum payment toward their student debt.

Employers that want to subsidize a student loan payment through a 401(k) matching contribution must pursue approval from the Internal Revenue Service. The process requires a private-letter ruling, given on a case-by-case basis. Abbott Laboratories was the first company to receive approval to use an employer match to help employees paying college debt. (Source: InvestmentNews).

Current law sets limits on linking certain workplace benefits. These restrictions have discouraged many companies from pursuing the loan subsidy.

Federal bill may expand benefits

In April, U.S. Senators Rob Portman (R-OH) and Ben Cardin (D-MD) introduced the Retirement Security and Savings Act of 2019. The bill includes several provisions to improve and expand the existing retirement savings system. A provision in the bill would make it easier for companies to contribute money toward paying employees’ student debt through the company 401(k) plan. The Senate has not yet voted on the bill.

317971

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.