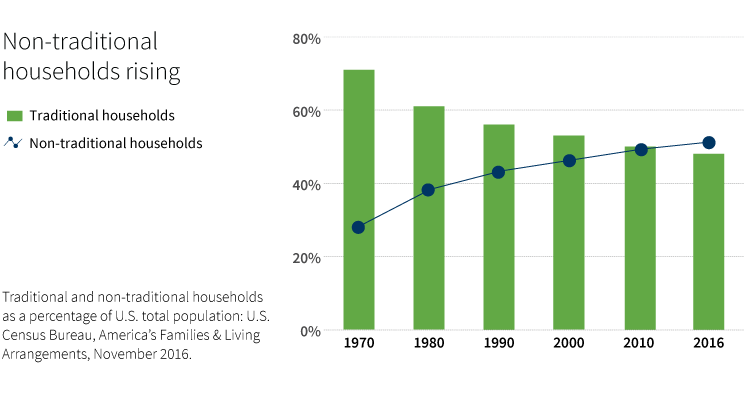

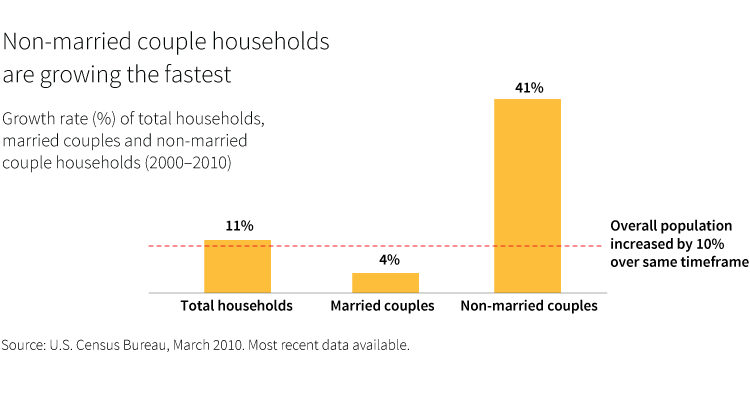

Over the last few decades, the number of non-traditional households has risen sharply while traditional households — defined as married couples — has decreased. In fact, one segment of non-traditional households has more than doubled since 2000 — non-married couples.

Because marital status plays a prominent role in financial rules governing retirement, insurance, income and estate taxes, individuals in non-traditional households may face unique challenges. Typically, a traditional married status provides automatic protections in areas of legal and property rights, and wealth transfer. But non-traditional households are not entitled to the same provisions, and often have specific planning needs.

A growing segment

The number of non-traditional households, defined as those headed by divorced and single individuals, or unmarried couples, has increased to 52% of all households today from 29% in 1970.

The fastest-growing segment includes non-married couples who live together. These households increased more than 40% during the last 10 years, compared with the 4% growth rate of married couple households.

Planning considerations for unmarried couples

Unmarried partner households may face a range of restrictions and limitations in financial planning. However, there are numerous strategies available to help them achieve their goals. Here are some planning considerations and strategies.

Retirement planning

- Beneficiary designations are critical. Unmarried partners cannot take advantage of the spousal default on retirement plans.

- Income projections should factor in the lack of Social Security survivor benefits. Also, many defined benefit pension plans will not provide automatic benefits to a non-spouse partner.

- IRA accounts do not provide for a non-spouse beneficiary to transfer ownership of an inherited IRA into his or her name.

Insurance rules

- Adequate life insurance is always critical.

- Consider an irrevocable life insurance trust (ILIT). This can be helpful as the unlimited marital deduction for estate tax purposes does not apply to an unmarried surviving partner.

- There are special considerations for health insurance. Some employer provided insurance plans may be taxable if provided to a non-married partner. Also, sometimes COBRA benefits are only allowed for an employee’s spouse, former spouse, or dependent child.

Income taxes

- Income-tax rules can differ for unmarried couples. Rules may vary regarding which partner can claim certain deductions. But there could also be an opportunity to shift taxable assets to the partner in the lower tax bracket.

- Unmarried couples may want to establish a separate paper trail for tax purposes on property.

Estate and wealth transfer

- There is no unlimited marital deduction for estate tax purposes. Planning for liquidity upon the death of a partner is important.

- Gift taxes may apply on the transfer of assets. Adding a partner to a real estate deed may result in an unintended taxable gift.

- There is a lack of automatic legal protections. Legal documents become more essential for unmarried couples, including a health-care proxy, durable power of attorney, wills, etc.

- A revocable trust may provide a more efficient way of wealth transfer. Simple wills could be challenged by family members.

- Consider a Domestic Partnership Agreement. Without the ability to legally divorce, this document can specify the division of assets.

About 28% of all households consist of one person. Single and divorced individuals also face specific challenges. Having the sole responsibility for household finances and saving for retirement, single individuals have different considerations. For more information and planning strategies for these and other non-traditional households, read Putnam’s investor education article, “Unique financial planning challenges face growing ranks of non-traditional households.”

304880

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.