One of the central pieces of the Tax Cuts and Jobs Act is corporate tax reform. Corporate tax rates were cut to a flat rate of 21% from 35%.

Tax rates lowered

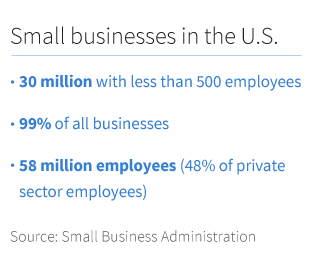

Still, most U.S. companies are not large corporations, but rather small businesses. The Small Business Administration defines a small business as one that employs less than 500 people. These businesses — often structured as S-Corps, Limited Liability Companies (LLCs), partnerships, or sole proprietorships — are generally taxed as “pass-through” entities. This means that the net business or partnership income is taxed at rates and brackets applicable to individual taxpayers.

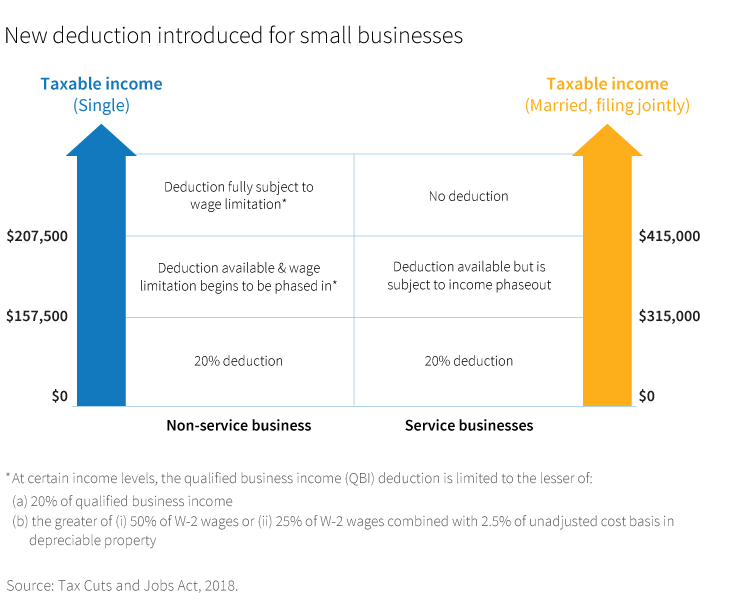

Smaller businesses are also affected by the tax reform legislation. The overall rates affecting individual taxpayers are reduced and would apply to pass-through entities. The law also provides for a new deduction available to businesses structured as pass-through entities — a 20% deduction for qualified business income.

The new deduction has some limitations depending on the type of business and household income. For example, professional service businesses such as law, accounting, finance, and consulting face limits when claiming the deduction.

The following table indicates how the deduction is applied.

Small business owners may consider meeting with their financial advisor or tax consultant to learn how to best optimize the new 20% deduction, and how the timing of income and other actions may impact the deduction, both positively and negatively. It may also be an opportune time to evaluate the status of a business. Business owners may want to consider what type of business structure or taxation method makes the most sense from a tax perspective. For example, an LLC may choose to be taxed as a flow-through partnership or as a C Corporation.

309988

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.