Many financial goals such as estate planning, educating children, or preparing for retirement, are universal, yet the path to get there often requires customized planning. Many couples, particularly same-sex couples who are not married, have to navigate some unique planning considerations.

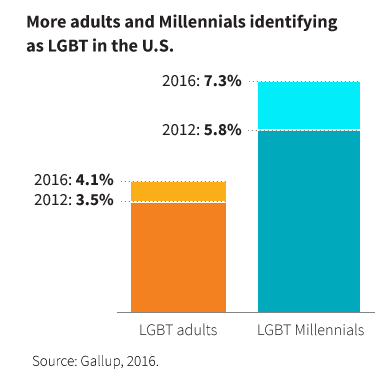

Today, more than 10 million Americans identify as lesbian/gay/bisexual/transgendered (LGBT). The number of LGBT Millennials rose to 7.3% in 2016, up from 5.8% in 2012. In a recent poll, 86% of LGBT people surveyed reported that they need wealth management services. Yet, two-thirds have not chosen a financial advisor.

In another survey of the LGBT community (Prudential, 2017), 45% of respondents said they need to follow a different path to meet the challenges of saving for retirement and other needs, and "urged financial advisors to consider the unique needs of LGBT clients."

Planning considerations

In the Prudential survey, 49% of participants were single, 7% were in a legally recognized relationship, and 34% lived together with no legal protections. The number of LGBT parents is also on the rise. The survey found that 23% of lesbians and 7% of gay men were financially responsible for a child under 18. Among Gen Y survey participants, 49% plan to have children.

Unmarried couples do not have access to the same legal rights and privileges as married spouses. But with proper planning and legal documentation, they can achieve many of the same rights and meet their planning goals.

- Establish beneficiary designations for retirement plans. Unmarried partners cannot take advantage of the spousal default on retirement plans. A beneficiary designation would avert the probate process that typically does not consider non-married partners as heirs.

- Plan for financial dependency. If one partner is financially dependent, then life insurance may be needed in case of death. Also, couples may want to consider long-term care insurance, especially if they are not likely to have children who could become caregivers in the future.

- Update legal documents. Unmarried couples lack the automatic legal protections and privileges of married couples. Legal documents and asset ownership decisions become even more essential. These documents include health-care proxy/medical directives, durable power of attorney, wills, trusts, etc.

State laws may influence planning

It is important to review and understand the distinction between federal, state, and local laws. In 2015, the Supreme Court made the landmark decision to legalize same-sex marriage in all 50 states. As a result, federal programs such as those administered by Social Security, the Internal Revenue Service, and Immigration Services that relate to married couples apply to everyone including same-sex married couples.

Prior to the federal ruling, only 36 states had legalized same-sex marriage. State laws needed to catch up to the federal mandate. Still, married LGBT couples need to understand state laws involving property ownership, parental and adoption rights, inheritance, and medical decision-making. There may be differences in state laws that could require additional legal documents from same-sex couples.

Understanding and organizing a financial plan as a married couple can be complex, and couples may want to be proactive and seek professional advice. The Supreme Court ruling on same-sex marriage highlights the need for couples to focus on financial and estate planning.

311913

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.