With the federal estate tax exemption now at a record high, fewer estates will receive an estate tax bill from the federal government. Still, estate planning remains critical as investors seek to manage the distribution of assets as well as meet any state tax requirements.

Indeed, more than a dozen states have death or inheritance tax laws.

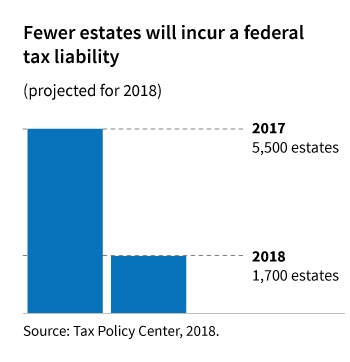

Most taxpayers will not owe federal estate taxes

The Tax Cuts and Jobs Act doubled the lifetime exclusion for federal estate and gift tax to $11.18 million in 2018. According to Tax Policy Center projections, the number of estates that will have a federal tax liability could fall to 1,700 in 2018, from 5,500 in 2017.

Many investors, however, will still need to plan for taxes at the state level. A total of 17 states, as well as Washington, D.C., that have a state inheritance or estate tax. Maryland has both taxes.

Estate planning considerations before year-end

- Create a “roadmap” document for family members in case of an unforeseen event. Family members will need to locate investment accounts, key documents, important contacts, online passwords, and specific instructions on how to proceed.

- Review/update plans and documents, including beneficiary designations on retirement accounts, life insurance policies, and annuities. Consider a revocable trust to help heirs avoid probate. In case of incapacitation or a health-related issue, someone needs to be designated with a power of attorney, health-care proxy, or health-care directive to make important health and financial decisions.

- Consider the impact of the increased lifetime exclusion on the operation of an irrevocable trust. Meet with your estate planning attorney to review and update existing trusts if necessary.

- Discuss the possibility of gifting assets to family members before year-end to take advantage of the annual gift tax exclusion. Give up to $15,000 per recipient ($30,000 for married couples electing split gifts). Read more in this recent blog about gifting while living.

- Consult a professional to avoid or reduce the impact of state-related death taxes. For example, life insurance may be an effective tool to create liquidity at death to pay state estate or inheritance taxes.

IRS clarifies potential impact of sunset provision on certain large gifts

Since the unified estate and gift tax exemption is slated to revert back to 2017 levels ($5 million indexed for inflation) after 2025, taxpayers have asked whether large gifts made after 2017 and before 2026 could be subject to a “clawback” provision. For example, assume a taxpayer utilized their entire lifetime gift tax exemption prior to the new law taking effect in 2018. The doubling of the lifetime exemption under the TCJA allows the taxpayer to gift an additional $5 million (plus an inflation allowance) without owing federal gift taxes.

However, if the law sunsets after 2025 and the lifetime exemption reverts to 2017 levels, investors want to know if the additional $5 million gifted under the terms of the TCJA would be “clawed back” into the estate of the taxpayer. Last week, the IRS issued proposed regulations addressing this issue, proposing that a “clawback” provision would not apply. Still, these are proposed regulations which are subject to potential amendment, and taxpayers should consult with a qualified estate planning professional when considering a lifetime gift.

Meet with a tax professional

It is important to consult a financial advisor to understand how estate tax and gift tax rules may affect your personal financial plan. Individuals considering advanced planning strategies around estates and gifting should work with a qualified estate planning attorney who has knowledge of their financial situation and goals. For more details about tax law changes and planning implications, read Putnam’s investor education piece, “A closer look at the current estate and gifting tax rules.”

Advisors, for more ideas around estate, tax, and financial planning, listen to our webcast replay “Year-end planning strategies under tax reform.”

314770

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.