With significant limits to tax deductions under the Tax Cuts and Jobs Act, many taxpayers are no longer itemizing deductions on their tax return and therefore are unable to claim a tax deduction for charitable donations. The vast majority of taxpayers are now claiming the standard deduction, which was nearly doubled under the recent tax law changes.

In fact, according to the Tax Foundation, only 13% of taxpayers have itemized deductions since tax reform, compared with 31% prior to the new tax law.

Given this shift amongst taxpayers, there may be other strategies to make donations and receive a tax advantage.

“Lump” charitable contributions

Instead of giving regularly each year, investors may want to consider combining three to five years’ worth of gifts into one year to itemize deductions for that particular year. Total itemized deductions would have to be greater than $24,400 for a married couple (higher than the standard deduction). For the other years, they would take the standard deduction of $24,400 for couples (or $27,000 if both are age 65 or older).

Taxpayers could invest their charitable gift in a donor-advised fund (DAF) in one year to claim the tax deduction and then make periodic gifts out of the DAF over the course of several years.

This example illustrates how this strategy might work.

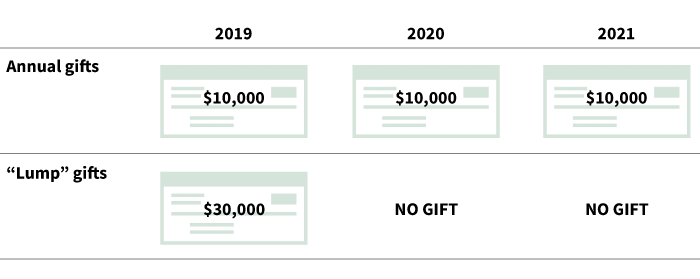

Combining charitable gifts

The example assumes a husband and wife, age 65, who donate $10,000 annually to charity. Other deductions include: $10,000 for state and local taxes (SALT) and $5,000 for mortgage interest. Their marginal income tax bracket is 22% and standard deduction is $27,000.

Result:

- With annual gifting, their total deductions equal $81,000 ($27,000 x 3 years).

- By lumping gifts, their total deductions equal $99,000 ($45,000 + $27,000 + $27,000).

- The result is a difference of $18,000, for a tax savings of approximately $4,000 (assuming a 22% marginal tax bracket).

The example is based on 2019 IRS figures and does not account for a higher standard deduction in 2020 and 2021 due to annual inflation adjustments.

Philanthropy is part of an overall plan

It is important to meet with a financial advisor or tax professional with an understanding of your personal financial situation. Depending on your overall tax plan, these strategies can have an impact on your financial goals.

advisor-only webcast

Advisors and their clients are still learning about new opportunities to reduce taxes under the recent changes to the tax code. Our upcoming advisor-only webcast will detail actionable strategies for year-end planning.

Register for our “Year-end planning strategies for financial advisors” webcast.

319178

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.