A year after the beginning of the pandemic, many families are focused on getting their finances back on track. This year, tax season feels more like back to school. For many families, students are returning to the in-person classroom for the first time in more than a year.

Families may want to consider reviewing their plans to fund education, whether it’s for K–12 or college costs. Goals may have changed, and time horizons may be pushed out a bit. Still, a plan review may help families ensure that their plan is on track to meet objectives. And tax season provides a good reminder that 529 savings plans offer significant tax benefits for families looking to fund college education.

Highlighting the long-term tax benefits of a 529

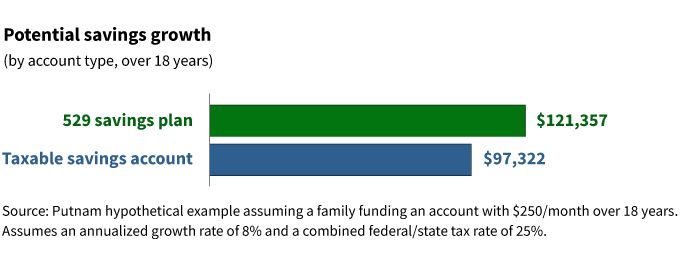

Because of the tax benefits, saving in a 529 plan may result in higher savings for college. To compare the after-tax performance of a 529 plan with using a taxable savings account, consider this hypothetical example:

- Parents fund a 529 account with $250/month for 18 years

- Assume the funds within the 529 grow at an 8% annualized rate

- The combined (i.e., federal and state) tax rate is 25%

Here is the possible outcome:

In this example, families saved nearly $25,000 from “tax drag” that can be used to offset college expenses. This assumes that the funds being withdrawn from the 529 plan are considered qualified expenses and avoid tax and penalty.

Other factors impacting college savings

Additional considerations have emerged with the changing landscape in Washington. Some families may wonder if they need to save for college.

Here are some topics to review with a financial professional:

- Review what is known about the Biden administration’s views on education and student loan forgiveness.

- Consider that tax rates may rise in the future. A 529 plan can provide tax relief as the assets grow tax free and qualified distributions are also tax free.

- In recent years, 529 plans have become more flexible and cover more than tuition, and room and board. Qualified expenses now include computers and internet service, qualified apprenticeships, and $10,000 per year for each beneficiary to pay for K–12 tuition. In addition, beneficiaries may use up to $10,000 to pay off student loans.

Consult with a financial professional

It’s important to meet with a financial professional who understands the family’s overall financial situation. Putnam has many resources families can use to review their college savings plans. Younger families may want to read our investor education piece, “College Planning for a Growing Family.” Families with children closer to attending college can reference the high school “Four-year action plan.”

325832

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.