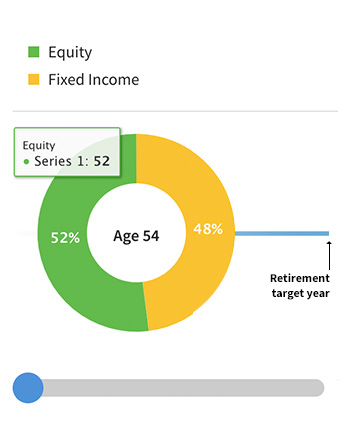

We manage the right risk at the right time

Putnam’s target date glide path is designed to help participants be more successful.

Research and resources

Committed to helping retirement plans succeed, we offer glide path research from our long tenured Global Asset Allocation team as well as product information for advisors and education for participants.

- Advisor resources

- Participant resources

TargetDateVisualizer®

See what separates target-date strategies. Find out why there's more to target-date strategies than just performance.

For advisors: Target-date strategies

Diversifying a portfolio across asset classes or risk sources is an effective way to reduce performance volatility and to take advantage of compounding through more consistent positive returns.

Set a course for retirement (participant brochure)

Portfolios diversified with multiple asset classes have been part of Putnam’s story since the launch of our first fund in 1937, and today Putnam is a leader in this area thanks to the managed diversification strategies of Putnam’s long-tenured Global Asset Allocation team.

The glide path less traveled

Successful glide path design must marry accurate estimation of quantitative inputs with efficient risk management. Using the most representative set of assumptions for the broadest segment of the plan participant demographic, we employ simulations to relate these assumptions to outcomes for the industry average glide path.

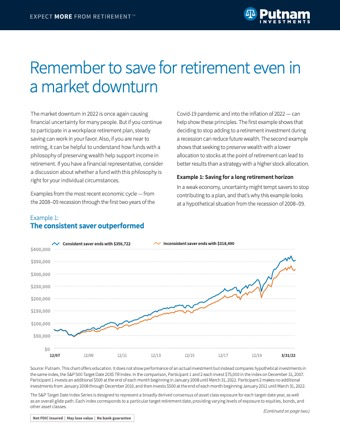

Remember to save for retirement even in a market downturn

The market downturn in 2020 is causing financial uncertainty for many people. But if you continue to participate in a workplace retirement plan, steady saving can work in your favor. Also, if you are near to retiring, it can be helpful to understand how funds with a philosophy of preserving wealth help support income in retirement.

Optimizing the glide path for a smoother landing in retirement

Retirement is one of American society’s most anticipated and eagerly sought milestones, yet the journey to and through retirement can be quite worrisome. Fortunately, with the help of plan features like automatic enrollment and automatic escalation, participants are contributing more to their retirement than ever before.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information discussed are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

The fund is a collective trust managed and distributed by Putnam Fiduciary Trust Company, a non-depository New Hampshire trust company. However, it is not FDIC insured; is not a deposit or other obligation of, and is not guaranteed by, Putnam Fiduciary Trust Company or any of its affiliates. The fund is not a mutual fund registered under the Investment Company Act of 1940, and its units are not registered under the Securities Act of 1933. The fund is only available for investment by eligible, qualified retirement plan trusts, as defined in the declaration of trust and participation agreement.

Consider these risks before investing: Our allocation of assets among permitted asset categories may hurt performance. Stock and bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, factors related to a specific issuer or industry and, with respect to bond prices, changing market perceptions of the risk of default and changes in government intervention. These factors may also lead to increased volatility and reduced liquidity in the bond markets. Growth stocks may be more susceptible to earnings disappointments, and value stocks may fail to rebound. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Default risk is generally higher for non-qualified mortgages. Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. International investing involves currency, economic, and political risks. Emerging-market securities carry illiquidity and volatility risks. Active trading strategies may lose money or not earn a return sufficient to cover trading and other costs. REITs are subject to the risk of economic downturns that have an adverse impact on real estate markets. Commodity-linked notes are subject to the same risks as commodities, such as weather, disease, political, tax and other regulatory developments and other factors affecting the value of commodities. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Efforts to produce lower-volatility returns may not be successful and may make it more difficult at times for the fund to achieve its targeted returns. In addition, under certain market conditions, the funds may accept greater volatility than would typically be the case, in order to seek their targeted return. There is no guarantee that the funds will provide adequate income at and through an investor's retirement. You can lose money by investing in the funds.

The Morningstar Rating™ for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36–59 months of total returns, 60% five-year rating/40% three-year rating for 60–119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Investors should carefully consider the investment objectives, risks, charges, and expenses of a fund before investing. For a prospectus, or a summary prospectus if available, containing this and other information for any Putnam fund or product, call your financial representative or call Putnam at 1-800-225-1581. Please read the prospectus carefully before investing.

Putnam Retail Management