As the Federal Reserve plots its actions and communications strategy for the gradual normalization of monetary policy, fixed-income investors face the challenge of anticipating the future course of interest rates.

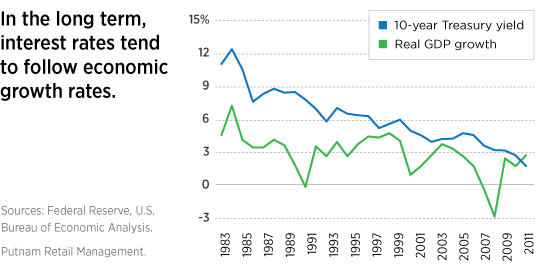

Economic growth influences interest rates

The long-term “equilibrium” interest rate of an economy is intimately linked to the economy’s overall growth potential when it is free of distortions, such as recessions or the energy supply shock of the 1970s, or the demand shock that followed the financial deleveraging crisis of 2008. The term “equilibrium” does not imply that these rates prevail most of the time. In fact, there can be large deviations from the equilibrium.

The relationship between economic growth and interest rates flows from demand for money. When economic activity accelerates, there is more demand for capital, causing the price of money — or interest rates — to increase. When the economy is sluggish or contracting, the price of lending decreases.

Understanding growth depends on analyzing labor

To calculate an economy’s growth potential, the most important variables involve labor — how much labor is available and how much capital is available for labor to utilize, which determines overall labor productivity. An economy’s growth rate is driven primarily by the change in labor supply and the change in labor’s productivity.

The United States faces growth challenges

When economic experts look at these factors in the recent history of the United States, most conclude that the potential U.S. growth rate is declining. That’s because the labor force is growing more slowly than it did in recent decades and because productivity has also been disappointing. We’ll look at these factors in subsequent posts.

If this view is correct, potential U.S. economic growth will be lower in the future than the approximate 3% level of the 30 years prior to the 2008 crisis. This would suggest that interest rates across the term structure would also be lower in the future than in recent decades. In turn, this outlook would have major consequences for income planning strategies.

Of course, rates would still likely be higher than current levels, which are being held below equilibrium by the Fed’s asset purchase programs.

284639

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.