Regarding Japan, we have expressed optimism in recent quarters about the potential economic gains from Prime Minister Abe’s reform program. In 2013, the government and the Bank of Japan unleashed a combination of expansionary policies focused on stimulating economic activity and weakening the yen to give Japanese exporters greater global competitiveness. Results so far have been mixed and, after an initial spurt, the economy has stumbled a bit. Japanese stocks, after leading the world in 2013, fell in the first quarter of 2014.

New tax hike sparks controversy

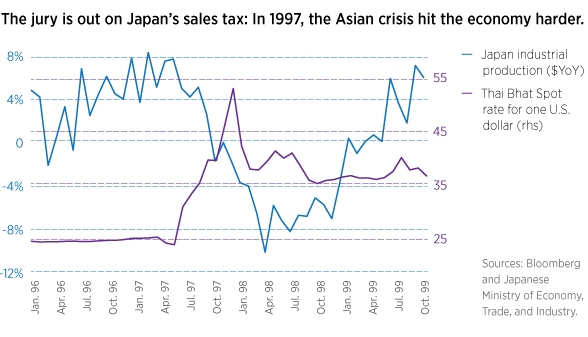

There will soon be fresh evidence to assess the reform program. The latest step — an increase in the rate of the national sales tax from 5% to 8% — went into effect on April 1, 2014. Skeptics believe it will undercut consumer spending and cause an economic tailspin, as in 1997 when the rate last increased. But senior officials within Japan’s Ministry of Finance and the Bank of Japan believe that the impact of the 1997 tax increase has been overestimated. They attribute more of the damage to Japan’s economy to the Asian currency and debt crisis, which broke out at the same time as the tax increase.

Proponents of the current tax hike look to the positive impact it is expected to have on government finances. Japan continues to have the highest national debt in the developed world, and without action, the situation will worsen as the country’s population ages and begins to shrink.

Policy action is possible

We will seek answers in the data soon to emerge, but we are generally disposed to favor Japanese stocks. If the economy performs well, it will make Japan’s debt more sustainable, which would put Japan in solid condition to contribute to global growth. If consumer spending takes a hit because of the sales tax increase, the Bank of Japan may take action. As a result, we are disposed to believe that Japan can join Europe and the United States as an engine of global growth.

288253

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.