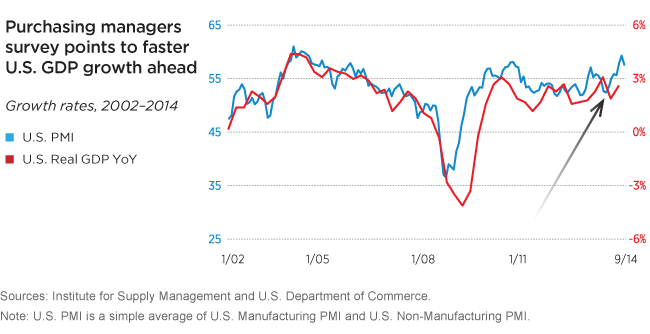

The U.S. economy is strong

We remain bullish on U.S. stocks because of the economy’s strength. At the same time, we favor a measured retreat from other risk positions. U.S. stocks are still our favorite asset class, but we have reduced an overweight to high yield. Liquidity in the high-yield market has been curtailed because of new financial regulations, and sharp losses during July indicated the risks facing investors, despite the snapback in August.

For our global positioning, we believe international equities continue to offer positive prospects — despite our concerns about deflation in our market outlook — because of easy monetary policy in Europe and Japan. While geopolitical risk increased during the third quarter, our research suggests that the military situations in Ukraine and the Middle East, and even the Ebola outbreak, do not appear to be significant factors for market performance.

Stocks require caution, but fundamentals remain favorable

U.S. equities advanced for a seventh straight quarter from July to September, although gains were modest and markets encountered turbulence as the quarter came to a close. In mid-September, the S&P 500 Index marked its 34th record close of the year, but quickly turned downward as investors became concerned about global geopolitical tensions and slowing growth in Europe and China.

Equity valuations today are in the top half of their average historic range. They aren’t extreme by any means, but stocks are more expensive than they have been in the past couple of years. We are seeing significantly fewer compelling valuation opportunities, and the market is closing in on three years without a statistical correction — that is, a decline of 10% or more from its peak.

In this environment, we continue to take a slightly more cautious approach to portfolio construction.

We believe the corporate earnings picture remains positive. Based on the most recent data from U.S. corporations, earnings growth has reaccelerated toward 10%, a level we haven’t seen in a few years. More important, revenue growth has started to rebound. Incremental margins were very strong — that is, earnings on every new dollar of sales were significantly higher than existing margins. Although margins are at record levels, we believe they can continue to expand as long as economic growth continues, even at a slow pace.

In the final months of 2014, the most notable risk for equities will likely be concern about U.S. monetary policy. As an anticipatory mechanism, the equity market could struggle ahead of the Fed’s first short-term interest-rate hike since 2006. History suggests that this is a challenge we will have to navigate carefully, particularly because this current cycle of monetary easing was unusually aggressive.

Non-U.S. stocks will continue to be influenced by a variety of factors in the months ahead, we believe. For Europe, these include the potential effects of the ECB’s new policy measures, the beneficial impact of a weakening euro, and the continuing evolution of the situation between Russia and the West. China’s growth, too, will continue to be an important factor. If the policy, currency, and geopolitical factors improve as we hope but China disappoints, that may deliver a mixed picture for European and even global stock performance.

We continue to pursue diversified fixed-income strategies

We are maintaining underweight exposure on the 5- to 10-year portion of the Treasury yield curve since we believe this area of the curve will be the most affected by the conclusion of the Fed’s bond-buying programs. Additionally, we will continue our efforts to minimize overall interest-rate exposure in the portfolios.

In our multisector portfolios, we plan to maintain our diversified mortgage, corporate, and sovereign credit exposure primarily through allocations to mezzanine commercial mortgage-backed securities (CMBS), high-yield bonds, and peripheral European sovereign bonds, respectively. In our investment-grade-only portfolios, we expect to continue emphasizing mezzanine CMBS as well as corporate bonds from various market sectors. Across all of our taxable fixed-income funds, we continue to believe it is an opportune time for taking prepayment risk, and we expect to keep the portfolios positioned accordingly. Historically, strategies that seek to benefit from prepayment risk have done well during periods of rising interest rates.

Globally, we believe the United States and the United Kingdom will be the economic growth leaders, as the ECB continues to provide liquidity to eurozone economies, seeking to stimulate growth in that region. With regard to rates, we think the outlook for Europe is more favorable than for the United States because the ECB is likely to keep rates low for some time while the Fed appears poised to begin raising rates. Thus, European bond markets look comparatively more appealing to us over the balance of this year and into 2015.

Download the full white paper, Putnam Capital Markets Outlook.

291370

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.