Many North American energy companies have borrowed significantly in the public debt markets to finance their operations, and many of the high-yield bonds in this space have lost value in recent months. As the price of oil has fallen, the economics have changed for these companies. At current price levels, profit margins are squeezed.

Still, within the energy sector, the impact of the price volatility varies.

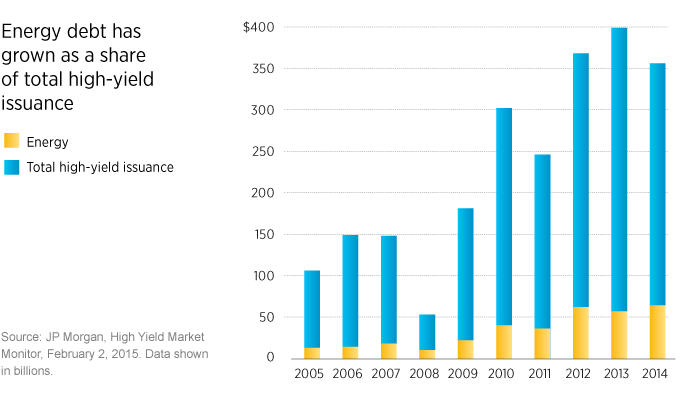

The Wall Street Journal reports that U.S. oil and gas companies have increased their borrowing by 55% since 2010, to an amount approaching $200 billion. Extracting and moving oil and gas is capital-intensive, so this debt is necessary for exploration and production (E&P) companies, and transportation companies, in particular.

As the price of oil has fallen, the economics have changed for these companies. At current price levels, profit margins are squeezed. Therefore, many of the high-yield bonds in this space have lost value in recent months.

The type of company varies within the sector

Within the sector there are E&P companies that extract energy from the ground, service companies that support the E&P companies, and transport companies, such as pipelines, that move the product. Of these, E&P companies face the most direct consequences of the price drop. Service companies, especially those that support producers with weak profiles, also experience an impact. Transport companies, however, see much less of the effect since energy must still be moved from producers to consumers.

Quality can also vary. Within these segments there are better-run, less-levered companies that should be more resilient than highly levered companies with less liquidity. We take these differences into account when assessing risk in the sector.

The pace of price recovery plays a major role

Should oil prices recover over the next year, we would not expect to see high levels of defaults in the high-yield market. A reason for this is that many companies have hedged their near-term production to lock in higher prices into the future.

However, if oil prices remain at or below $50 for a prolonged period of a few years, an uptick in default risk becomes more likely, though the risk would probably remain manageable in the context of historical default levels. We continue to monitor the situation in high yield closely.

294755

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.