In 2015, weak global growth, the tightening of U.S. monetary policy, and the appreciation of the dollar all created major headwinds for emerging markets (EM).

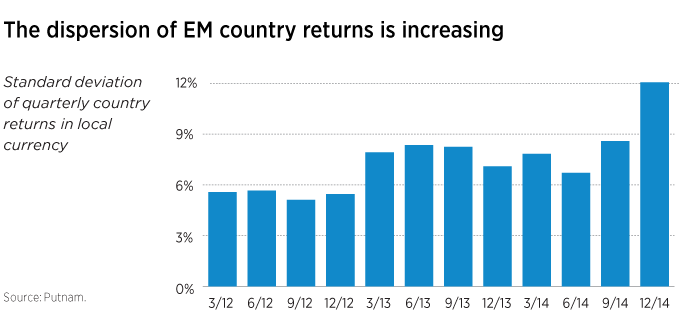

However, we believe all emerging markets should not be lumped together. Recent evidence shows much greater dispersion in the performance of these markets — and this is a new trend.

The dollar does not dominate everywhere

It’s crucial to dispel the myth that U.S. monetary policy is the most important consideration for all EM countries. The EM picture is vastly different today than in the mid- to late-1990s, when nearly all EM countries issued debt in U.S. dollars. Today, many countries issue more local currency debt.

Economic differences abound

Consider the so-called “BRIC” countries — Brazil, Russia, India, and China. A decade ago, market consensus was that these countries advanced in synchronized fashion.

Today, however, vast differences exist —

- Brazil and Russia are major commodity exporters hurt by low oil prices and other raw materials.

- Brazil’s economy is expected to contract 1% this year, while inflation runs at 8%.

- Russia is also dealing with economic sanctions and a decline in the value of the ruble as fallout of the war in Ukraine.

- China, meanwhile, is a massive commodities importer, but is attempting to refashion its growth model to a more domestically driven economy.

- India may offer the most intriguing opportunity, with pro-business government policies and a central bank led by an MIT-trained economist who once worked at the International Monetary Fund.

Despite the headwinds buffeting the asset class in general this year, we believe that select emerging markets offer attractive investment potential for the global investor.

296064

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.