In many ways, the global economy at the end of 2015 is still struggling to define itself outside the financial crisis of 2008. Economic recovery has been uneven across the globe: The United States is moving right along; Europe appears to have just turned the corner into recovery; and China may be teetering on the verge of harder times as its head of economic steam is now dissipating.

Growth forecasts fall short of long-run averages

A careful analysis of growth patterns in developed-world economies shows that a recovery to higher growth rates is by no means impossible — particularly in the United States. But in our macroeconomic research, we also find that potential growth is likely to be lower than the long-run averages for a number of major developed countries due to structural economic impediments and population dynamics.

A qualified recovery emerges

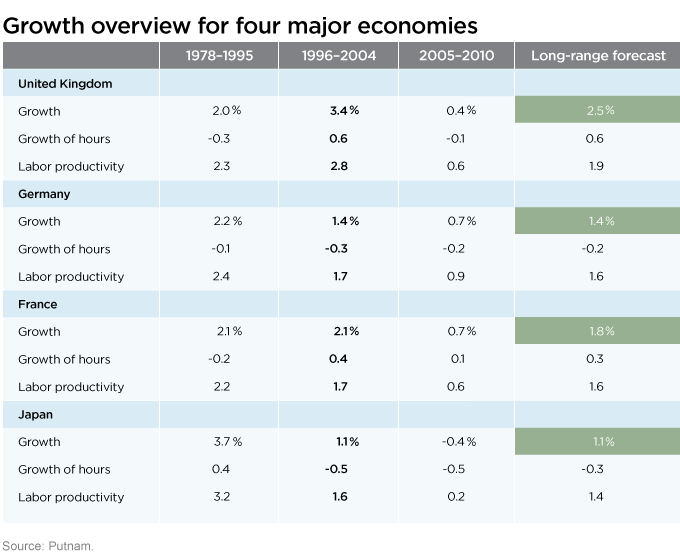

Our research shows that the United Kingdom, Germany, France, and Japan are, with some qualifications, headed toward a recovery, but one that is below each country’s long-range “normal” economic growth rate. As the table indicates, our forecast for growth sees each country recovering approximately to its 1996–2004 average but remaining below its 1978–1995 average — with the exception of the United Kingdom, where the projected recovery situation is reversed.

A mix of temporary and long-term issues

In all cases, the growth slowdown from 2005 to 2010, a period that includes the financial crisis and Great Recession, as well as some years of relative strength before the crisis occurred, appears to be severe. But if the demand side of each of the economies under examination is able to recover, we believe the slowdown will prove to be a temporary phenomenon. Put another way, we think the supply side of each of these economies may be able to respond to renewed demand and convert it to growth.

Breaking down labor productivity

Another immediately apparent factor we note concerns the impact of demographics on labor’s contribution to growth. As Figure 1 shows, growth in Germany and Japan suffers from a decline in the growth of hours worked, which is one of two major factors that our analysis identifies as a source of growth. As we discuss further in our published research, the second major factor of growth, labor productivity (LP), has three internally complex components: capital deepening (CD), labor quality (LQ), and total factor productivity (TFP).

Together, these factors make growth rates a dynamic function of sometimes conflicting, sometimes mutually amplifying inputs.

Financial professionals: Read Putnam's new study, Low-gear growth ahead for developed economies, for our research and analysis on non-U.S. developed-market growth.

298066

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.