- Auto enrollment has fueled 401(k) participation among millennials, but their contributions still lag older workers'.

- Most (85%) of millennials view their investment decisions as an expression of their social and political values (Source: U.S. Trust, 2016).

- 90% of millennials in a recent study noted they are interested in pursuing sustainable investments as part of their 401(k).

Plan design features like auto-enrollment continue to raise participation rates among workers who have access to an employer-sponsored defined contribution plan such as a 401(k).

Nevertheless, deferral rates still vary significantly among different age groups, indicating that some workers may not be taking advantage of a company match or might not understand the long-term benefits of consistent saving.

Auto-enrollment boosts participation

In a recent study, Bank of America Merrill Lynch found that auto enrollment lifts 401(k) participation among all age groups, and particularly among millennials. In the survey, the number of millennials enrolling in a plan for the first time jumped 55% compared with a year earlier, largely due to auto-enrollment. Across all age groups, participation increased 37%.

Still, contribution deferral rates vary and several industry studies found that millennials participate at lower deferral rates than older workers.

Could the grass be greener?

Millennials may not be contributing at higher rates because they feel limited by their financial situation. In the early stage of a career, they may feel constrained by their salary level or other financial responsibilities, such as college debt.

They may also feel constrained by their plan choices. Recent surveys point to a growing interest among millennials in socially responsible, ESG, or sustainable investment choices. Research from Morgan Stanley found that 90% of millennials are interested in pursuing sustainable investments as part of their 401(k)s.

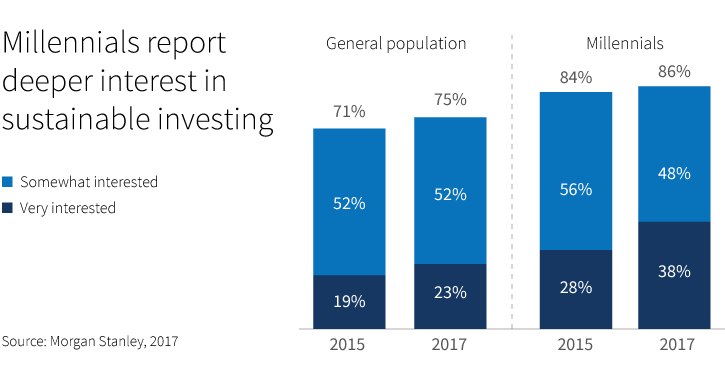

Millennials are leading the way in this nearly $9 trillion market, and are twice as likely as the overall pool to invest in companies or funds that target social or environmental outcomes, the report stated.

Millennials’ interest in sustainable investing grew substantially to 86% in 2017 from 84% in 2015, the report found. The percentage of millennials stating that they were “very interested” jumped to 38% in 2017 from 28% in 2015.

A growing number of investors are factoring sustainability issues into their investment decisions, notes the Global Impact Investing Network. In fact, a 2013 study of wealthy millennials by the Spectrem Group noted that 45% of those surveyed consider social responsibility when making investment decisions.

Plan sponsors are trying a variety of ways to encourage millennials to invest more in workplace savings plans. Two that show promise involve plan design and investment choices. Auto-enrollment has demonstrated the ability to increase participation among millennials, and sustainable investment choices may be attractive to them as well.

307989

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.