For many investors with taxes top of mind, the new year means a fresh look at the tax landscape.

While most significant changes from the Tax Cuts and Jobs Act (TCJA) were implemented in 2018, there are some provisions that only recently took effect and many changes that resulted from inflation adjustments.

Key tax figures

A first step for investors in tax planning for the coming year is to determine their tax bracket. Putnam’s “2019 tax rates, schedules, and contribution limits” can be a useful reference to review with a financial advisor.

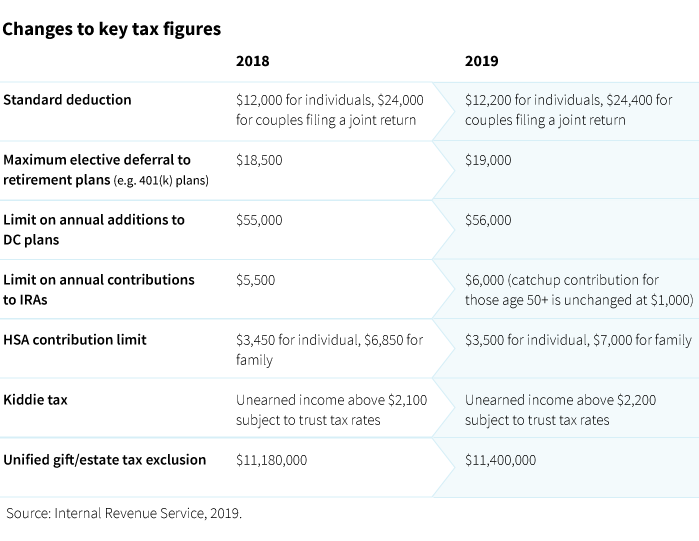

Most tax figures remain unchanged in 2019, although investors will note some changes to tax brackets and other figures to account for inflation. For example, contribution limits increased for health savings accounts and retirement savings plans, including 401(k)s and IRAs.

New provisions effective January 2019

Two provisions from the TCJA are slated to change in January 2019, including the medical expense deduction and the tax treatment of alimony payments.

- Medical expenses. The TCJA preserved the deduction for medical expenses and reduced the threshold for deducting expenses from 10% to 7.5% of adjusted gross income (AGI) for tax years 2017 and 2018. Beginning in 2019, however, the threshold for deducting medical expenses reverts to 10% of AGI.

- Alimony payments. Beginning in 2019, alimony payments are no longer deductible and alimony received is not considered taxable income. This change goes into effect with divorce agreements finalized after 2018. For additional details read our recent blog post, “Two provisions under the TCJA will change for 2019.”

Planning considerations

Given the changes in the tax rates and contribution limits, investors may want to discuss tax-smart strategies in the areas of retirement saving and estate planning.

- Review retirement plan contributions. If an investor is maxing out 401(k) contributions for 2018, they may want to consider deferring an additional $500 to max out for 2019. The same applies for IRAs with the contribution limit increasing from $5,500 to $6,000. Investors may also want to take advantage of the tax benefit of increasing contributions to a health savings account.

- Plan for deductions. With the dramatic increase in the standard deduction under the TCJA and limits to other popular deductions, investors should plan accordingly. If possible, consider maximizing deductions into one tax year when itemizing. For example, “lumping” charitable tax deductions into one year may provide an advantage for investors wishing to itemize.

- Review estate plans. In light of the increased lifetime exclusion amount, it is timely to review current estate plans. Estate planning remains an important part of an overall financial plan to ensure the orderly transfer of wealth. Putnam’s investor education piece, “A closer look at current estate and gifting tax rules,” may be helpful. It explains how the TCJA affects estate planning and explores the advantages of gifting while living.

315303

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.