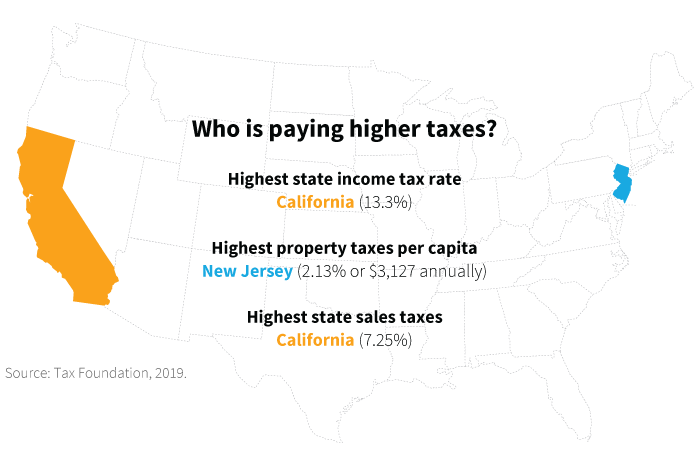

Recent tax law changes have increased the state tax burden for residents of high-tax states. Changes that limit deductions have made planning for state and local taxes more important.

Prior to tax reform, many taxpayers could deduct state and local taxes (SALT) on their federal tax return, which partially mitigated the impact of state taxes. SALT primarily consists of state income taxes and local property taxes. (In lieu of deducting state and local income taxes, taxpayers can opt to deduct state and local sales taxes.)

With the new limit on the SALT deduction set to $10,000 annually, residents of states with higher taxes may find they can no longer itemize deductions.

Some trusts may alleviate state income taxes

Incomplete non-grantor trusts (INGs) may help high-income taxpayers avoid state income taxes on certain assets. These trusts are considered “incomplete gift” trusts since contributions to the trust are not taxable gifts for federal gift tax law because the donor/grantor typically retains certain rights, such as the right to change the trust’s beneficiaries, hence the “incomplete” nature of the gift.

- For an ING to be effective, the assets must be legally sited in a state that has no state income tax, the grantor must typically not be the only beneficiary, and all distributions from the trust are generally approved by a “distribution committee” that consists of the grantor and at least two other beneficiaries. The “distribution trustee” must at all times be composed of enough members to avoid giving any member of the committee, including the grantor, the unilateral power to benefit himself or herself.

- Since the ING trust is established as a non-grantor trust it is considered a separate taxable entity and taxed accordingly.

- Assets held in the ING trust are managed by the out-of-state trustee and are typically intangible assets such as investment accounts that can be transferred to a different jurisdiction (unlike physical property such as real estate).

- Income generated on assets within the ING trust can avoid state income taxes. But federal income taxes apply at trust tax rates (where the highest marginal tax rates ) once income retained within the trust exceeds $12,750.

- There are nine states that have no income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. The most popular states utilized for these types of trusts are Nevada (NINGs), Delaware (DINGs), and Wyoming (WINGs).

Certain taxpayers may find a benefit

A taxpayer who may benefit:

- Is already in the highest marginal income federal income tax bracket

- Holds highly-appreciated intangible assets such as a stock portfolio or stock options (selling a stock or exercising an option within the trust can avoid state income taxes)

- Is not relying on income produced by the property transferred to the ING — income distributed to trust beneficiaries will be taxed based on their state of residency

- Has the means to absorb the cost of establishing and maintaining the trust arrangement

Other considerations

States may take legislative action in the future to tax assets held in these trusts. For instance, in 2013, New York lawmakers passed a state law that prevents the avoidance of state taxes through the use of INGs. This law treats ING trusts established in other states as grantor trusts, and it taxes a New York resident grantor on the income, regardless of whether it is distributed from the trust or not.

State tax authorities may also challenge the transfer of an asset to an ING trust and its subsequent sale shortly thereafter as a tax avoidance scheme. To mitigate this risk, the grantor should consider holding the appreciated asset within the trust for a longer period of time before selling the asset.

There may be key legal differences in states offering these trusts. For example, there are some subtle, but potentially significant, differences between INGs in Delaware and Nevada.

Legal advice is recommended. This type of trust planning can be very complex. Consultation with a legal professional who is knowledgeable on these strategies is critical.

317721

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.