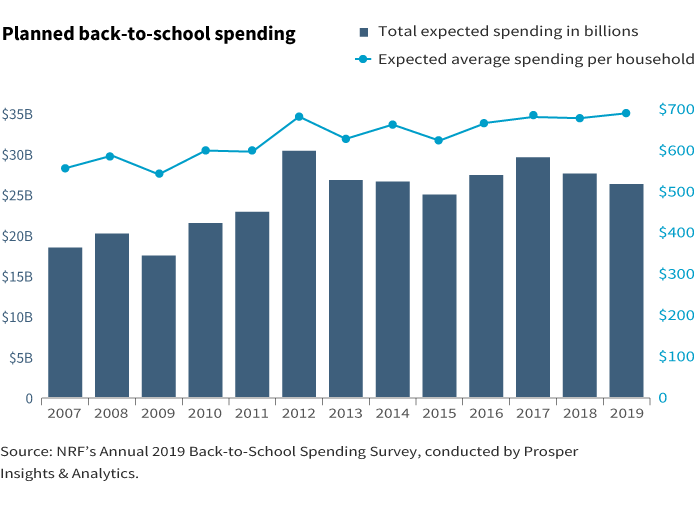

Families will spend record levels during the 2019 back-to-school season.

According to the National Retail Federation, families with children in elementary through high school will spend an average of $696 for back-to-school items. Families with college students will spend $976, which tops the 2017 record.

Should families spend or save?

College tuition is rising at nearly double the rate of inflation. The cost of a four-year public college could exceed $200,000 for babies born today, according to The College Board. Higher costs could lead more families to seek financial aid. Among the class of 2018, for example, 69% of college students took out student loans, and now face an average monthly payment of $393.

What can families do today to avoid debt?

Consider careful spending today but make a plan for the future. Families may need to save for college, private K-12, or both. Begin with a cost projection. Putnam’s college cost calculator can help set goals and its comparison tool can help families select the most efficient savings vehicle.

For example, a 529 plan offers tax advantages, no income or age-restrictions, control of assets, flexibility when plans change, and better financial aid treatment.

Start early, contribute often

Here are some examples of savings strategies.

- The Smith family has a newborn and starts saving right away. Working with their financial advisor, they determined that they must contribute $340 each month to their account to pursue their goal. That is less than the current average of monthly debt referenced above.*

- The Jones family waits 10 years to start saving. They can still meet their goal, but they have to contribute much more — $1,219 — each month. *

The earlier that families begin contributing, the easier it will be to pursue college savings goals and avoid debt. It is important to note that systematic investing does not guarantee a profit or protect against loss.

Get everyone’s help

Another strategy is to involve other family members.

- Consider a grandparent who makes a lump-sum contribution of $15,000, leaving the parents to contribute $226 a month in order to meet the savings goal.†

Seek advice

With many options for saving and other commitments that may challenge a family’s ability to save, it’s important to have a plan. It's never too early to start saving. Making a commitment to saving early may result in having more options later. Read more on this topic in Putnam's education piece, "Early college planning for a growing family."

A financial advisor can help families structure a savings plan and update the plan as it gets closer to the start date for college. For more information read Putnam’s education piece, “Strategies to make the most of college savings.”

*These charts are for illustrative purposes only and not intended to be representative of past or future performance. The Jones family saves $340 monthly for 18 years. The Smith family saved $1,219 monthly for 8 years. Assumes a hypothetical 8% annual return compounded monthly.

†This chart is for illustrative purposes only and not intended to be representative of past or future performance. The Jones grandparent makes a lump-sum contribution of $15,000 today. The Jones parents contribute $226 each month. Assumes a hypothetical 8% annual return compounded monthly.

318119

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.