A decelerating economy, volatile financial markets, and escalating trade tensions could force the Fed's hands on interest rates.

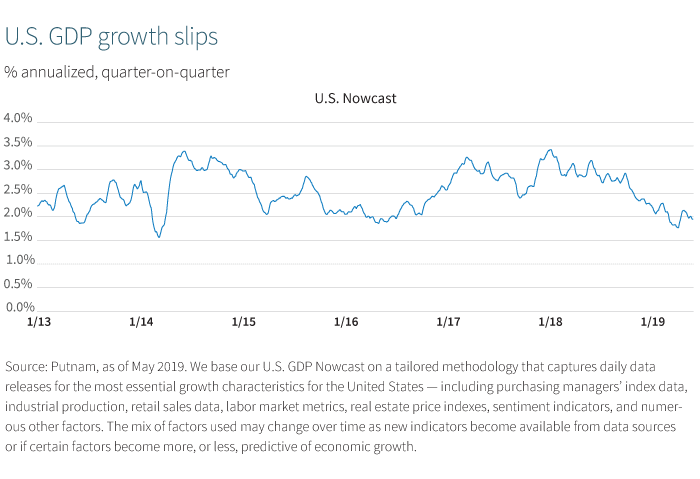

The U.S. economy is facing headwinds with a number of elements placing stresses on economic expansion. First, the trade war and the Trump administration's approach to protectionist tariffs are creating uncertainties among businesses. Second, corporate investment is not doing very much even after the corporate tax cuts. And third, higher rates are exerting pressure on debt that is tied to the front end of the Treasury yield curve, especially consumer credit.

Fed rate cut in the cards

In recent weeks, the trade war has escalated. Rising trade tensions between the United States and China have ricocheted through financial markets; risky assets tumbled in the second half of May, and investors fled to safe-haven investments. The Treasury yield curve inverted further, and there were calls in the market for the Federal Reserve to cut interest rates. Fed Chair Jerome Powell provided some soothing words, and risky assets rallied sharply.

We are not at all convinced this is a rerun of late 2018 when the Fed's decision to shift to a neutral stance laid the groundwork for the strong rally in risky markets in the first quarter of 2019. We can't blame the weakness in risky asset on interest rates. Rates have been falling, and the Fed has been busy stressing patience and neutrality. Markets are reacting to the reality of slower growth and to the prospects of a further slowdown.

As we have noted before, an inverted yield curve is a powerful signal that something is awry. While an inverted curve alone does not cause or predict a recession, it is a signal of serious, potential stresses in the asset markets. Those stresses, if unchecked, can threaten the economy's prospects. The easiest way to get some steepness into the curve is for the Fed to cut rates. But generating a steeper curve by increasing long-term rates, while short rates remain unchanged, is simply implausible at this time since neither a rise in inflation expectations nor a jump in the equilibrium global real rate seem remotely likely.

We expect a rate cut soon; the Fed will likely lower its policy rate by 50 basis points by the end of 2019.

Speaking at a Fed conference in Chicago in early June, Powell said the Fed "will act as appropriate" to sustain economic expansion. That was the dovish signal asset markets were looking for. We expect a rate cut soon; the Fed will likely lower its policy rate by 50 basis points by the end of 2019. But there is still a hurdle to be crossed; we will need to see more financial market turbulence or a run of weaker data, or both.

If the president finds a way to make peace on the various trade battles, if global the economy recovers, and if asset markets track sideways or higher, then the chances of a rate cut will fall. But right now, we believe that is unlikely. Too much damage has been done to a global economy already facing headwinds, and the domestic U.S. economy, facing its own challenges and trade war uncertainties, is not strong enough to shrug off these headwinds.

May jobs report disappoints

The sharp decline in the pace of hiring in May was a surprise. The government reported that employers added just 75,000 jobs last month, a far cry from what economists had expected. Although the unemployment rate held steady at 3.6%, the lowest in about 50 years, average hourly earnings increased by just 3.1% from a year earlier, less than projected. The slowdown in job creation was quite broad across the economy.

And once again, there are no signs of widespread wage pressures. We don't see this U.S. payrolls report as so weak that it will force the Fed's hand on rates; rather, it illustrates that the economy is slowing. We think the trade wars are weighing on the labor market. Overall, this is consistent with our view that the economy is weakening a little and that the headwinds from the trade war are raising the risks. In this context, it makes sense to think that the Fed will cut rates, but it doesn't mean the June meeting will bring that cut.

Recession risk trends higher

We believe the risks to the economy are rising. Growth is slowing, and policy risks (trade) are increasing. The markets for risky assets are nervous. It would not take much to tip the economy into a weaker path. In this sense, the probability of a recession on our favored models appears much more likely to rise than to fall.