In 2005, his final year as Chair of the Federal Reserve (a position he held for almost two decades), Alan Greenspan delivered his penultimate Humphrey-Hawkins testimony to the Senate and said, "For the moment, the broadly unanticipated behavior of world bond markets remains a conundrum. Bond price movements may be a short-term aberration, but it will be some time before we are able to better judge the forces underlying recent experience." By that time the Fed had already increased the federal funds target rate six times, lifting it from 1% to 2.5%. In spite of this policy, the 10-year Treasury yield was virtually unchanged, remaining in the low 4% range where it had been stuck for most of the previous two years.

Just one month later, while serving as a member of the Board of Governors of the Federal Reserve, Ben Bernanke gave a speech in which he said: "… over the past decade a combination of diverse forces has created a significant increase in the global supply of saving — a global saving glut — which helps to explain both the increase in the U.S. current account deficit and the relatively low level of long-term real interest rates in the world today." Upon assuming his role as the next Fed Chair the following year, he would reiterate this view several times. In early 2013, with 10-year Treasury yields sitting just below 2%, Bernanke gave another speech at a conference sponsored by the San Francisco Fed, saying: "If, as the FOMC anticipates, the economic recovery continues at a moderate pace … then long-term interest rates would be expected to rise gradually toward more normal levels over the next several years."

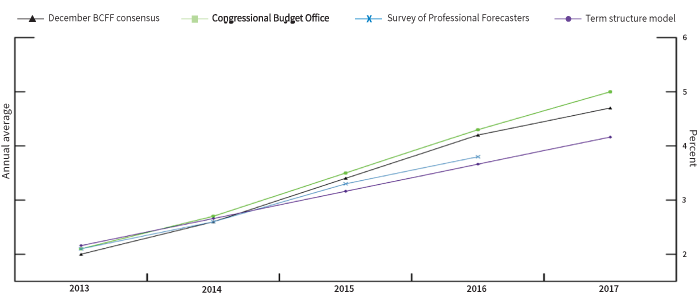

2013 projections of higher 10-year Treasury yields

Forecasts of Treasury yields presented by Fed Chair Ben Bernanke to San Francisco Fed

Source: Federal Reserve.

The speech was accompanied by the chart (above) illustrating several yield forecasts for coming years. All of them expected yields to be above 4% by 2017. For reference, the 10-year Treasury ended 2017 with a yield of 2.4%

What is past is prologue

While most prognosticators (at least the honest ones) would admit to feeling a bit of schadenfreude at the expense of others' bad forecasts, we point out this chronic undershoot of yields relative to forecasts simply because so many investors are expecting negative nominal bond returns in 2022 as the Fed begins to tighten monetary policy. A measure of positioning in 10-year Treasury futures published by the CFTC (Commodity Futures Trading Commission) shows that currently non-commercial traders (which the CFTC defines as those that are not using futures for hedging purposes) are about as short as they have ever been over the past decade, with the exception of the run-up to the "Powell Pivot" in late 2018. (The Powell Pivot refers to the Fed's decision to pause after a series of rate increases considered too aggressive.)

Treasury futures indicate bond bearishness

Net non-commercial combined positions in 10-year Treasury futures contracts

Source: CFTC. Units are the number of futures contracts, adjusted for options.

The current "conundrum" may be less about the level of nominal rates and more about the level of real rates (or nominal rates adjusted for inflation). There is still a fair bit of noise in the inflation data related to the pace of reopening around the world and supply chain issues that may be exacerbated by policy responses to the Omicron variant,* and the Fed still seems puzzled. The real yield on 10-year TIPS (Treasury Inflation-Protected Securities) is stuck stubbornly at -100 basis points despite ultra-easy monetary and fiscal policy and a U.S. economy likely to average real GDP growth of close to 6% in 2021. We would venture to say that Bernanke's global savings glut hypothesis is instructive even to this day, a full 15 years since the coining of the term. His proxy for the flow of this global excess savings into the United States — the U.S. current account deficit — is again about as large as it was when he gave that speech in 2005.

Global savings glut has returned to levels seen when Ben Bernanke introduced the term

U.S. current account balance ($ billions, quarterly)

Source: U.S. Bureau of Economic Analysis.

The search for yield

Perhaps we shouldn't be so surprised by this. After all, the U.S. 10-year Treasury is still one of the higher-yielding developed market government bonds. Many foreign investors, particularly in Europe and Japan, experience a solid yield advantage from U.S. Treasuries even after hedging their currency exposure. Global regulatory rules, such as Basel III for banks and Solvency II for insurance companies, have risk-weighted capital charge rules that cause financial institutions to favor holding Treasuries on their balance sheets. This is all part and parcel of a way of quietly taxing savers in what Stanford economists Edward Shaw and Ronald McKinnon first referred to as "financial repression" in 1973.

In the waning days of 2021, the politics of inflation jeopardized President Biden's "Build Back Better" initiative in Congress, and thus it also seems likely that issuance needs from the Treasury will be largely scaled back in 2022 relative to expectations. Although the Fed will be debating the merits of balance sheet runoff in the first half of 2022, it is unlikely that they will be material net sellers of Treasuries anytime soon.

Bonds still offer balance

We find ourselves again in a position of having to remind clients that the reports of the death of

60/40 stock/bond balanced investing are wildly exaggerated, at least for the time being. It is instructive that 10-year Japanese Government Bonds (which have yielded pretty close to zero for most of 2021) have had a total return of about 0.30% this past year. Adjust that return with a volatility of around 1%, and you have an asset with a Sharpe ratio almost exactly equal to the long-term average of the U.S. bond market. With the application of a prudent bit of leverage, you could have earned a nice return in 2021, as well as a great complement to an equity allocation.

We continue to expect negative stock/bond return correlation and the benefits of diversification to continue, even in the face of sticky inflation, into early 2022. And the global search for yield continues to be driven by Bernanke's global savings glut, which keeps us from being bearish on assets like corporate credit.

* We believe inflation is likely to remain stubbornly high for longer due to higher home prices feeding into owners' equivalent rent (with a lag) and a slow recovery in the labor force participation rate. We plan to comment more about that in Q2 22.