- Over a nearly 100-year sample, intermediate-term government bonds have offered risk-adjusted returns that slightly exceeded domestic large-cap stocks.

- High-quality bonds are valuable to reduce portfolio volatility and maximize risk-adjusted returns.

- These results are possible through the “free lunch” of portfolio diversification. Combining these two uncorrelated asset classes provides a more efficient return.

It is fair to say the first half of 2022 has been tough for bond investors. The 10-year U.S. Treasury note yield has moved from 1.52% to start the year to more than 3.47% in mid-June. Since bond prices move in the opposite direction of yields, most fixed income investments have experienced negative returns year-to-date. Understandably, this has led some investors and plan sponsors to ask: “Is it still an appropriate time to own bonds?”

In this post, the first of a three-part series, we will make a case for long-term investment in both stocks and bonds. Subsequent pieces will consider related questions: “Are bonds too risky right now?” and “Can active management help navigate a rising-rate environment?”

Below, we share insights gained from studying long-term performance and what they mean for portfolio allocations.

The 100-year perspective

It’s easy to see why investors might question a bond allocation in the current interest-rate environment if they’re viewing bonds on a stand-alone basis. However, it is important to view high-quality bonds with a broader perspective. Aside from performance, they serve a valuable role in portfolio construction to reduce portfolio volatility and maximize risk-adjusted returns.

We believe a study of the history of capital markets may generate insights that can help investors in the future. When studying stocks and bonds, we are fortunate to have nearly a century of data to judge. The following table includes the performance of U.S. intermediate-term government bonds (measured by the Ibbotson U.S. Intermediate Term Government TR Index) and large-cap stocks (measured by the Ibbotson U.S. Large Stock TR Index).

Government bonds have better long-term risk-adjusted returns (Sharpe ratio) than stocks

| 1/1/1926–3/31/2022 | Intermediate government bonds | Large-cap stocks |

| Average annualized return | 4.97% | 10.38% |

| Annualized standard deviation | 4.30% | 18.61% |

| Sharpe ratio | 0.40 | 0.37 |

| Stock-bond correlation | 0.05 |

Sources: Morningstar, Putnam.

Over long cycles of both rising and falling interest rates, bonds delivered positive, mid-single-digit returns for investors. Also, bonds delivered these returns with a relatively low annualized standard deviation. In fact, when comparing these two asset classes individually, intermediate-term government bonds have offered risk-adjusted returns that slightly exceed those of domestic large cap stocks.

The optimal multi-asset portfolio

While a stand-alone look at each asset class provides some insight, investment managers must also understand how various asset classes interact with each other in a combined portfolio. Because stocks and bonds do not tend to move in the same direction over full market cycles, owning them together may provide a more efficient return than an investor could achieve by owning either asset class individually. Some investors call this the “free lunch” of diversification. Combining these two uncorrelated asset classes provides a more efficient portfolio return.

Again, using our 100-year sample, we examine various combinations of stocks and bonds to determine which allocation maximizes the portfolio’s risk-adjusted return.

Combining bonds and stocks in a portfolio has historically generated higher risk-adjusted returns

Sources: Morningstar, Putnam. Returns from January 1, 1926–March 31, 2022.

Among the allocation combinations charted above, we observe that the point of maximum portfolio efficiency (or highest Sharpe ratio) is roughly 80% bonds and 20% stocks.

In summary

Informed by nearly 100 years of data, we see evidence that intermediate-term government bonds have offered risk-adjusted returns slightly higher than domestic large-cap stocks. In addition, these bonds have proven valuable when combined with large-cap stocks. Through the power of diversification, high-quality bonds have historically helped managers improve portfolio efficiency by increasing risk-adjusted returns.

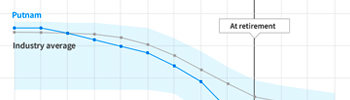

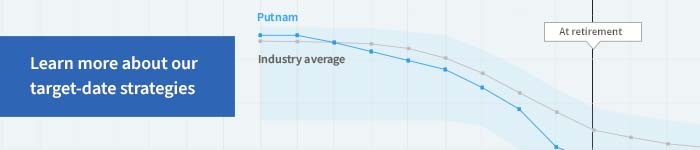

Retirement plan investors seeking portfolio efficiency can access diversified strategies in target-date funds. These funds use a glide path design to adjust allocations to stocks and bonds over a long time horizon.

Next in the series

Many investors believe we are destined for a prolonged period of rising interest rates. In our next article, we will examine the topic “Are bonds too risky right now?” We will take a critical look at the historical experience of the early 1960s through the early 1980s to glean possible insights for bond investors today.

330365

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.