Traditional target-date funds are likely to dominate flows

Traditional target-date funds remain as the qualified default investment alternative (QDIA) of choice for most retirement plans, but newer features of managed accounts (MAs) and advisor managed accounts (AMAs) are bringing innovations to the industry.

Target-date Funds' 401(k) market share

Percentage of total 401(k) market, year-end

Source: Tabulations from EBRI/ICI Participant-Directed Retirement Plan Data Collection Project. Most recent data available.

Personalization and managed accounts have become increasingly important in defined contribution retirement plans, as they allow employees to tailor their retirement savings to their individual needs and goals. Savers are asking, if I can have personalized Netflix, Uber, and Amazon (just to name a few) experiences, why can't I have a personalized or dynamic QDIA for my retirement plan?

Since the Pension Protection Act of 2006, target-date funds have been the dominant vehicle for QDIA flows, with the majority of plan sponsors opting for these strategies in lieu of MAs or AMAs. Today, however, advances in technology have created a new question: How can QDIA 2.0, a combination of managed accounts, advisor managed accounts, and TDF personalization, build on the base of this success?

QDIA 2.0 is emerging as data collection improves

Now that personal data about savers can be gathered via recordkeepers or third-party intermediaries, advisors and plan participants are showing an appetite for customized retirement planning.

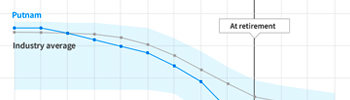

For years, allocation decisions have been based on the single factor of participant age. The ability to supplement age with contribution rate, company match information, and participant balance, makes it possible to construct a more-informed target-date fund.

These personalized TDFs may help both engaged and disengaged savers achieve better outcomes than a traditional TDF. Better outcomes is defined as sufficient savings to meaningfully replace income while lowering variability of outcomes. Having more data raises the probability of achieving better outcomes.

Additional data will be used to determine differences in the financial situation of savers who are in the same target-date vintage based on age. As differences are determined, adjustments to the accounts of savers within the vintage may be made. As a result, a single vintage may have as many as five variations to meet the various needs of the savers within the vintage.

Managed accounts and advisor managed accounts have the potential to have more than five variations per age group. Generally MAs and AMAs are built from a plan's core menu. Using more data inputs and many or all of the investments in a plan's core menu, are ways that MAs and AMAs are different from personalized target-date funds.

While an improvement on the traditional TDF, personalized target-dates stop short of all the benefits delivered by managed accounts or advisor managed accounts. The additional inputs utilized and engagement provided by MAs and AMAs may be well suited for more sophisticated financial planning situations.

In conclusion, personalization and managed accounts may play a useful role in 401k plans by equipping employees to align their investments with their overall financial circumstances. In fact, the two could even play a complementary role, with personalized target-dates introducing customization early and paving the way for managed account adoption as the employee approaches retirement. Employers and employees may want to consider the benefits of personalization and managed accounts when choosing and administering a 401k plan.

Personalized TDFs and MA/AMAs come with increased cost and added services. As these costs are analyzed, the availability of multi-factor versus single-factor allocation decision making, may hold much promise in improving investor outcomes.

We can help

Since MAs and AMAs are model portfolio based, optimization of the model being used can contribute to participant success. Visit our Portfolio Solutions Group page to see how we can help you look inside retirement portfolios for potential unexpected risks. Our services are available for TDF or managed account analysis. Our DCIO Team would like to discuss your views on QDIA 2.0 and personalization.

332952

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.