While it is generally not advisable to withdraw funds from a retirement account before retiring, it’s important to understand the alternatives for avoiding an early withdrawal penalty.

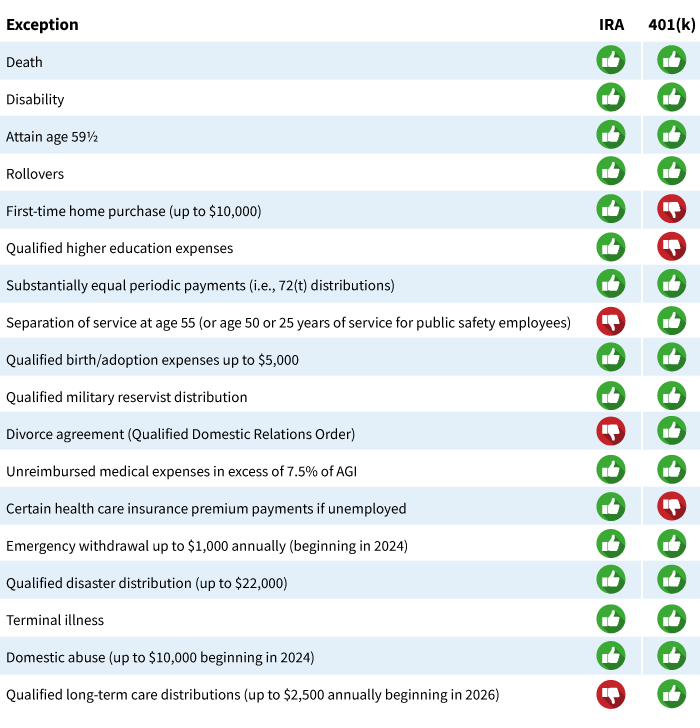

Not only are the rules different in the case of an IRA versus an employer retirement plan in some cases, recent legislation added a number of new exceptions to the list. For example, as a result of SECURE 2.0, plan participants and IRA owners will be able to request an emergency distribution of up to $1,000 beginning in 2024.

Here’s a look at the exceptions to the 10% early withdrawal penalty and differences between IRAs and 401(k)s.

Exceptions for 401(k) accounts also generally apply to 403(b) and 457 accounts. There may be other, less common, situations for avoiding the 10% early withdrawal penalty on a distribution. Examples include an IRS levy, a corrective plan distribution, or a dividend pass-through from an ESOP. For more information, consult IRS publication 590-B, Distributions for Individual Retirement Arrangements; IRS Topic 558, Additional Tax on Early Distributions From Retirement Plans Other Than IRAs; or IRS Topic 557, Additional Tax on Early Distributions From Traditional and Roth IRAs.

Planning considerations for avoiding a 10% penalty

- Proceed with caution before establishing at a 72(t) distribution schedule from your IRA or retirement plan. While it can be an effective method for generating income and avoiding a 10% early withdrawal penalty, there are strict guidelines that must be followed. For example, the payment schedule must continue for five years or until age 59½, whichever is longer. Taking premature distributions from an IRA requires careful consideration. Early withdrawals may result in higher current taxes and reduce the amount of money ultimately available during retirement. For more information, see “Looking for a way to supplement your income?”

- Spouses under age 59½ who inherit an IRA may want to remain as a beneficiary of the inherited IRA instead of transferring the funds to their own IRA. Unlike non-spouse beneficiaries, spouses have the option of treating an inherited IRA as their own or remaining as a beneficiary on the account. A spouse under age 59½ who remains as a beneficiary can avoid a 10% early withdrawal penalty through the death exception. If desired, once the surviving spouse reaches age 59½, they could opt to transfer the assets into their own IRA. This would especially make sense if the surviving spouse was younger than the deceased spouse to delay RMDs as long as possible.

- Workers leaving their company at age 55 and before reaching age 59½ may want to request a penalty-free distribution from their retirement plan before rolling those funds into an IRA if they need access to some of the funds. This will avoid the 10% early withdrawal penalty.

Overall, if funds are needed for an immediate expense, it’s generally better to exhaust other options before considering an early withdrawal from a retirement account. Even if there is an exception to the 10% penalty, taxable income will be generated when taking a distribution from a traditional retirement account. With less retirement funds available later in life, longevity and inflation risk may be more of a challenge.

334078

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.