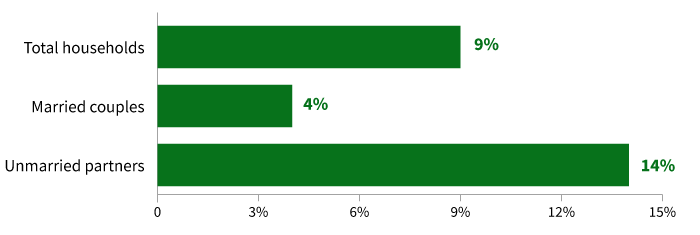

While married couples still represent most households in the country, their share of total households has been decreasing. According to recent Census Bureau data, married couples represent 46% of total households. As a comparison, during the 1980s, 60% of all households in the U.S. were married couples. In contrast, one of the fastest-growing types of households is unmarried partners. Currently, about 9 million households are composed of unmarried partners. While fewer in number compared with married couple households (almost 60 million), the growth of these households has outpaced married couples by a large margin over the last decade.

Growth of married couples vs. unmarried partner households (2010–2020)

Source: U.S. Census Bureau, “Married Couple Households Made Up Most of Family Households,” May 2023.

Marital status drives many rules involving retirement, insurance, income and estate taxation, and government programs like Social Security. Consequently, unmarried partners face unique challenges. For example, married couples receive protection in areas of legal and property rights, medical decision-making, and wealth transfer. Unmarried partners generally are not entitled to the same advantages. For example, unmarried partners lack spousal benefits for Social Security and Medicare and may not be able to access medical information on their partner.

Here are some examples where unmarried partners face financial planning challenges due to:

- Lack of Social Security or Medicare spousal benefits

- Inability to make unlimited gifts between partners

- Being subject to unfavorable treatment for federal estate taxes (no access to the portability provision for the lifetime estate tax exclusion)

- The denial of access to critical health-related information about a partner in case of an emergency

As a result, these couples need to understand potential issues from a financial planning perspective and pursue strategies to achieve better outcomes for the well-being of their partners and their finances.

Learn more about the key planning considerations in “Unique financial planning challenges face growing ranks of non-traditional households.”

Key planning areas for unmarried partners

Retirement

- Beneficiary designations are critical: Since unmarried partners cannot take advantage of spousal default on retirement plans, a beneficiary designation avoids the probate process that would generally not consider non-married partners as heirs if no will exists.

- Lack of Social Security survivor benefits needs to be considered: Additionally, many defined-benefit pension plans will not provide automatic benefits to a non-spouse partner.

- IRA limitations may reduce RMD options: The opportunity for a spouse beneficiary to transfer ownership of an inherited IRA into their name does not extend to a non-spouse beneficiary. This may prevent a non-spouse beneficiary from delaying or reducing required minimum distributions (RMDs) after the death of the account owner.

Insurance

- Adequate life insurance is critical: This is particularly important if one partner is financially dependent on the other.

- Consider an irrevocable life insurance trust (ILIT): This can be helpful since the unlimited marital deduction for federal estate tax purposes does not apply to an unmarried surviving partner.

- Special considerations for health insurance: In some cases, employer-provided health care may be taxable if provided to a “non-family member." Additionally, a partner who loses their job must consider that COBRA benefits are only eligible for “qualified” beneficiaries such as an employee’s spouse, former spouse, or dependent child.

Income taxes

- Income tax issues: There may be tax filing-related issues such as who gets to claim certain deductions, for example.

- Establish a separate paper trail: Unmarried partners should track ownership of certain assets such as real estate to record each partner’s basis for tax purposes.

Estate planning and wealth transfer

- No unlimited marital deduction for estate taxes exists: For larger estates, planning for liquidity to handle taxes upon the death of the first partner is even more critical.

- Gift taxes may apply on the transfer of assets: For example, adding a partner to a real estate deed may result in an (unintended) taxable gift.

- There is a lack of automatic legal protections for unmarried couples: Legal documents as asset ownership decisions become even more essential for unmarried couples. These include health care proxies and medical directives, powers of attorney, wills, and trusts.

- A revocable trust may make sense: These trusts may provide a cleaner method for transferring assets at death. Simple wills may be challenged during the probate process by other family members.

- Consider a domestic partnership agreement: This agreement can specify division of assets in the absence of legal divorce proceedings.

There may be a few opportunities in tax planning

Unmarried partners may benefit from their status in certain tax-related situations since there are still areas of the tax code where the “marriage penalty” still applies.

For example, the 3.8% surtax on investment income applies for single filers above modified adjusted gross income (MAGI) of $200,000, while the threshold for married couples filing a joint tax return is $250,000. In addition, once capital losses have been applied to capital gains, excess losses are limited to offsetting $3,000 of ordinary income. This limit is the same for single filers and married couples filing a joint tax return. Also, there may be opportunities to shift certain income to a partner in a lower tax bracket.

To learn more about these tax and planning considerations, see “Unique financial planning challenges face growing ranks of non-traditional households.” When considering actions that may impact your overall financial plan, or before establishing a trust, it is important to consult with a financial professional and tax expert.

334079

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.