The pending expiration of most tax provisions at the end of 2025, including the lifetime estate and gift tax exclusion, is prompting the review of estate plans. For individuals potentially impacted by these scheduled tax changes, it may make sense to take action now – such as with gifting strategies.

Of course, no one can predict what the future holds and what action Congress may take before 2026. But these tax figures may change. In particular, the life exclusion for gifts and estates is scheduled to be reduced in half.

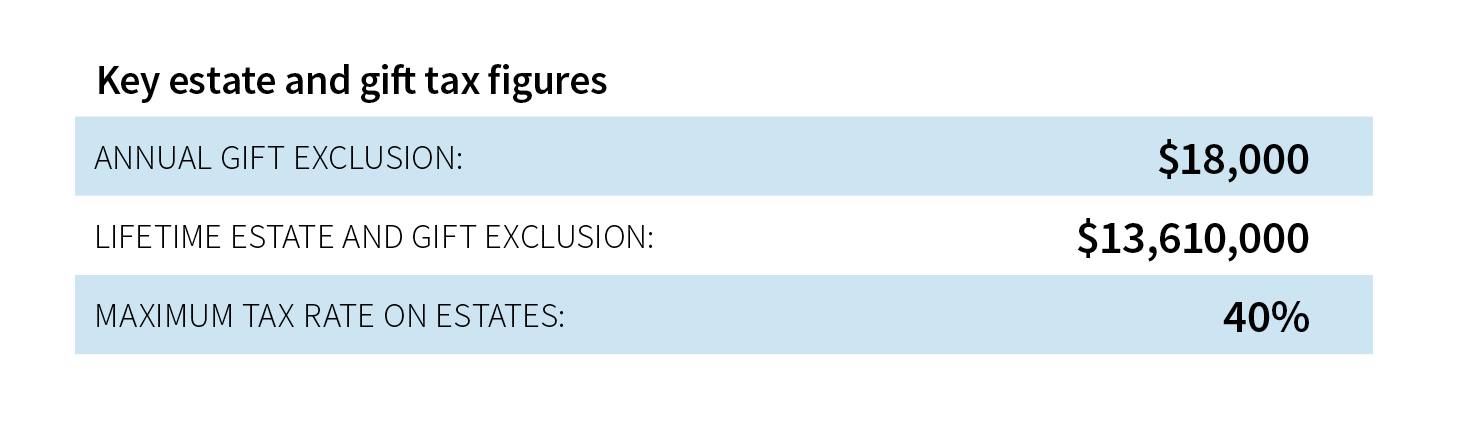

Source: IRS, 2024 figures.

Annual and lifetime gifts

The annual gift exclusion allows unlimited gifts ($18,000 per individual, $36,000 for married couples electing to split gifts) to as many recipients as desired.* Once a gift to one recipient exceeds that amount, a gift tax return must generally be filed to report a taxable gift. Even though the gift may be considered “taxable,” there would not necessarily be a tax payment due. Instead, the amount of the gift exceeding the annual limit would be subtracted from the lifetime exclusion.

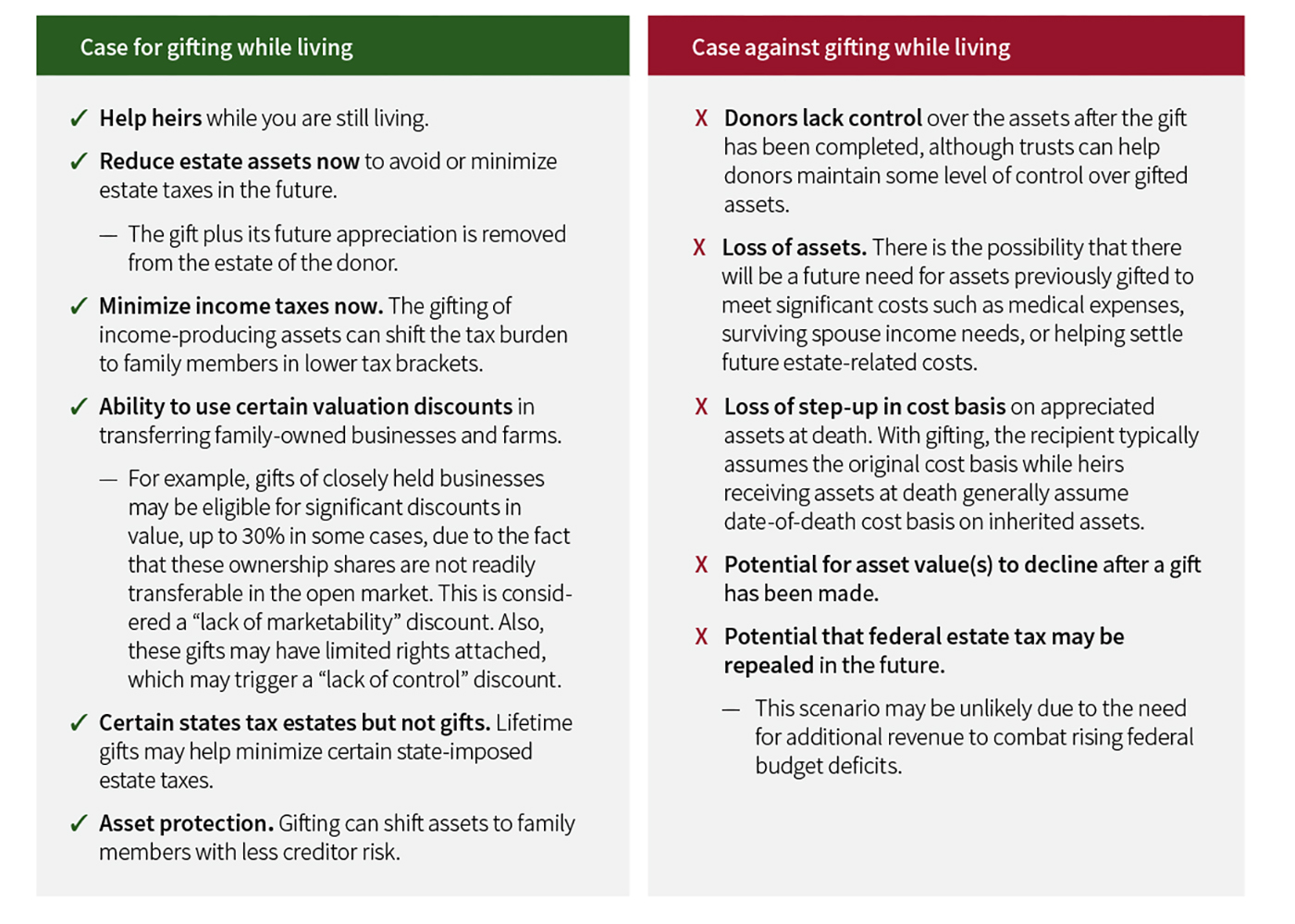

Gift during lifetime or leave assets to heirs at death?

This is a typical decision for those looking to transfer wealth to other family member. Does it make more sense to make gifts while I’m living or leave assets to family members at my death? There are a range of different considerations depending on the specific circumstances. For example, making a lifetime gift may be appealing to someone who wants to see the impact of their gift while they’re living. This may include making a gift to help a family member put a down payment on a house. However, it’s important to remember that gifts are generally irrevocable. The loss of control over those assets must be carefully considered.

Here's a deeper look at some of the considerations:

One of the biggest considerations from a tax perspective is the step-up in cost basis at death. While certain assets left to heirs at death benefit from a step-up in cost basis, when lifetime gifts are made, the cost basis of the asset carries over from the giftor to the recipient. For highly-appreciated assets this tax treatment of assets left at death can provide significant cost savings. For example, consider a stock held in a taxable account (i.e. not in a retirement account) that was purchased at $20 per share. At the death of the owner the stock is valued at $200 per share. As a result of step-up in cost basis at death the amount of appreciation based on the value of the property at death ($180 a share in this case) escapes capital gain taxation on this appreciation when the asset is sold.

In general, individuals who are not likely to be subject to estate tax may want to pursue strategies to take advantage of step-up on cost basis. For example, they may want to avoid transfers of appreciated property while living. This may be less of a consideration for certain assets (like a family vacation property) that will be passed on to successor generations without being sold. While tax ramifications are important to consider, there may be other factors that take precedent. Lastly, while there have been some conversations in Congress to repeal or limit step-up in cost basis at death, there has not been enough support among lawmakers to enact a change.

*There is a special provision which allows front-loading of five year’s worth of gifts into a 529 plan. For example, an individual could gift $90,000 into a 529 ($18,000 x 5 years) this year without having to file a gift tax return. That gift would represent annual gifts for the next five years.

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.