For financial strategies, interest-rate moves matter.

Many financial planning strategies are linked to IRS interest rates, and rates can have a significant impact on the viability of certain strategies.

Higher interest rates will generally benefit certain strategies, but lower interest rates will benefit other strategies. While we have experienced a decline in interest rates for decades, the recent shift to a higher-rate environment has wealth advisors rethinking certain financial planning strategies. For example, wealth transfer strategies such as grantor retained annuity trusts (GRATs) or intrafamily loans may not provide the same benefits as they did just a couple of years ago.

Key IRS interest rates to watch

Applicable Federal Rate (AFR). The IRS publishes three interest rates each month: a short-term rate (under 3 years), a mid-term rate (3 to 9 years), and a long-term rate (over 9 years), based on average market yields from securities of different maturities (U.S. Treasury bills). The AFR is used as a guideline for determining interest rates on private loans as well as for many other tax-related applications.

IRS section 7520 rate. Published monthly, this rate is equivalent to 120% of the federal AFR mid-term rate rounded to the nearest two-tenths of a percent. The rate is often referred to as the “discount” or “hurdle” rate for determining the value of certain property interests in split interest trusts, including charitable trusts and GRATs.

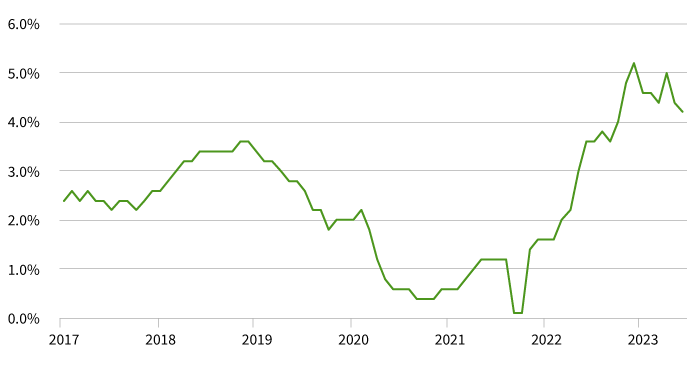

IRS 7520 rate

Planning strategies for a higher-interest-rate environment

Charitable remainder trust (CRT). A donor receives regular interest payments from the trust over a certain time frame, while benefiting from a tax deduction when the trust is funded. Any remaining share within the trust after the term ends is transferred to the charitable organization. The IRS requires that at least 10% of the assets (based on a present value calculation) funded within a CRT will eventually be remaindered to the charitable organization.

There are two types of CRTs: a charitable remainder annuity trust (CRAT) and a charitable remainder unitrust (CRUT). A trust beneficiary will receive a uniform payment from a CRAT, while the payment stream from a CRUT may vary based on the value of the assets held within the trust. Higher interest rates will generally result in a higher charitable tax deduction for the donor when the trust is funded.

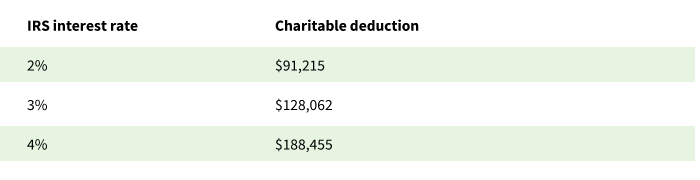

Example: Charitable deduction will vary by the prevailing IRS interest rate (i.e., §7520 rate):

Source: Putnam research. Assumes $500,000 is contributed into a charitable trust with a 5% annual payout to the beneficiary over a term of 20 years.

Qualified personal residence trust (QPRT). This trust allows families to transfer ownership of a residence while enabling the owner to continue living there over the trust term. Executing this strategy correctly can remove the value of the asset from the owner’s estate. Once a residence is placed into a QPRT, the owner can stay in the house until the specified date, at which time ownership is transferred to the beneficiary. If that occurs while the original owner is still alive and wants to remain living in the house, then they would have to pay rent at a fair market value to avoid a taxable gift.

Higher interest rates will generally result in a lower taxable gift when the trust is established, which can allow the owner to remove other assets from their estate through gifting.

Seek advice when considering timely strategies

Overall, interest rates have increased since the Federal Reserve began its monetary tightening cycle. Although the Fed took a pause on tightening at its June meeting, Chair Jerome Powell indicated more rate hikes are likely at future meetings to rein in inflation. It’s important to consult with a financial professional or tax expert before taking advantage of strategies that will impact tax and estate plans.

For more information on interest rates and planning, see “Planning ideas with potential higher rates on the horizon.”

334267

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.