- Multiple studies show that Americans are broadly unprepared financially for retirement.

- A successful retirement savings plan combines informed investor behavior with optimal plan design and investment options.

- It is important to consider investment needs across the participant population.

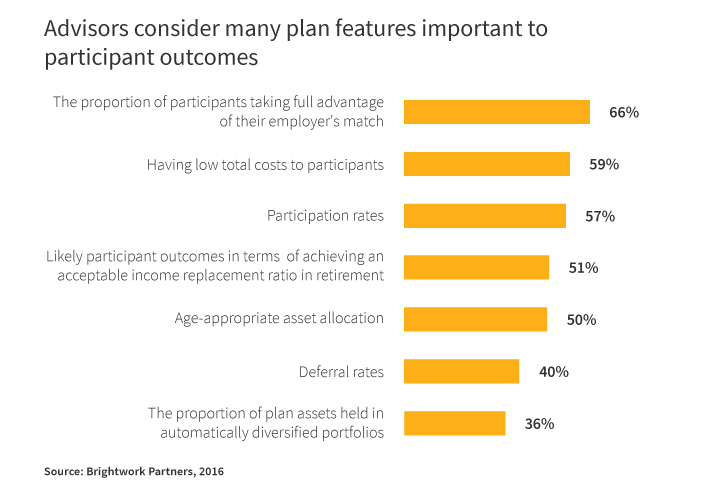

A growing number of advisors cite participant outcomes that are reflected by income replacement in retirement as an important measure of retirement plan effectiveness.*

Outcomes are the consequence of more than just investment returns. Plan features including auto enrollment, auto-increase, employer match, participant deferral rates, and investor education all work together to drive improved participation, savings rates, and ultimately accumulation of retirement assets.

The importance of saving adequately

Future retirees must set savings goals, make the necessary savings to replace working income in retirement, and take responsibility for selecting a process aimed at maximizing results by both growing and later preserving retirement assets. If investors do not save enough during their working years, chances of a positive outcome are slim. The higher the savings rate, the higher the probability of success.

Auto features and education play critical roles

Plan advisors and sponsors must work together to consider the age demographics and salary ranges of the participant population to design a plan that can fit the needs of a range of participants. This begins with investment education and incentives for maximizing participant contributions including making enrollment and investment decisions easy.

Auto enrollment, a company match, and automatic increases in deferral rates are all factors in improving the chances that participants reach their retirement savings goals.

Target-date funds are a compelling investment option

The other critical piece of plan design is having investments that complement needs across the participant demographic. Target-date funds resolve this issue by providing professional, disciplined, risk-managed investing based on where the participant is on the glide path to retirement. When participants have long time horizons, the primary goal is to accumulate wealth by investing aggressively and maximizing savings. Glide paths maximize growth potential at the accumulation phase. As participants get closer to retirement, the need for accumulation is increasingly balanced by the need to preserve assets. Target-date funds can manage this process seamlessly for participants.

Plan sponsors also see benefits

A primary benefit for plan sponsors is that employees who save enough are able to retire on schedule, which may also decrease costs for employers, more than making up for increased plan costs. Giving participants the education and investments they need to be successful can increase positive outcomes across the board.

* Study by Brightwork Partners LLC, 2016.

308330

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.