- A traditional gauge of 401(k) success typically measures inputs

- Analyzing projected outcomes can drive retirement plan design changes

- Most plan participants in a recent study do not intend to make changes to their plan investments (Cogent 2018)

As memories of Super Bowl LIII fade, excitement is building around March Madness. The NBA and NHL seasons charge toward the playoffs. MLB spring training is at the plate, and golfers know that early April is time for the Masters.

In every sport, every season, every event, the key metric is the score. Why? Because we want to know the outcome.

Companies that sponsor workplace savings plans such as a 401(k) also have a responsibility — to their employees and to their bottom line — to keep score. To do this, plan sponsors need a meaningful metric to define success.

What does success look like?

Many plan sponsors use a scoring approach that tracks participation or savings rates. But these are inputs, not outcomes. Tom Brady may throw 40 completions in a game, but the Patriots could still lose in the end.

It has been said, “If you cannot measure it, you cannot improve it.” If companies are not tracking the outcome of their 401(k) plan, they have no way to monitor if the plan is successful. In sports, scorekeeping systems are well defined and accepted across each league or association. The 401(k) industry could do the same, by adopting an easy-to-understand methodology.

Formulating a consensus metric

The ultimate 401(k) success score could be based on — quite simply — income replacement. In other words, Is this plan on track to meaningfully replace income for a significant number of its participants?

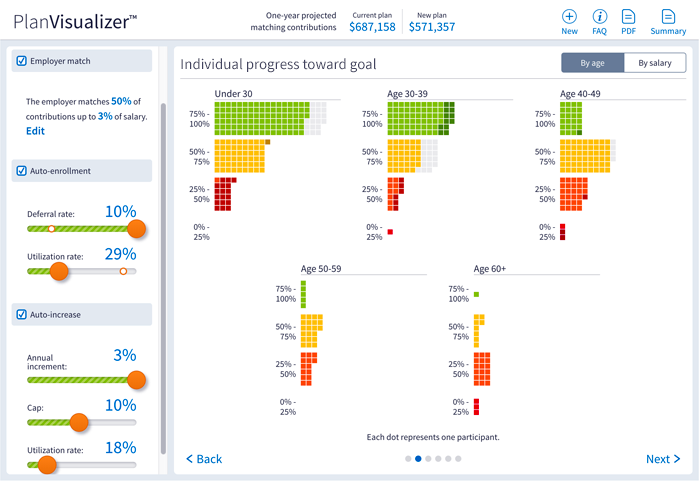

If we look at four inputs for each eligible participant, and the impact of these metrics on outcome, we can begin to formulate a score. These are the data points that contribute to the scoring calculation of Putnam's PlanVisualizer.

- Age: Plans with predominantly younger or older participants present structural opportunities and challenges to a plan’s success score

- Salary: Higher earners will require greater savings to successfully replace income in retirement

- Account balance: Helps determine whether participants are close to meeting their goals

- Individual contribution rate: Reveals how quickly participants may achieve their savings goals

By factoring a plan’s matching contribution into the data set, we can determine the plan’s success score on a scale of 0 to 100. This method uses participant and plan data to determine an income replacement score. Plan sponsors can make adjustments to plan design that, when modeled, can show how each change can raise the score.

Data-driven results

For years, companies and recordkeepers have invested a lot in educating retirement savers on the benefits of saving in a 401(k), but participation rates and retirement readiness have advanced only a bit. In fact, a recent survey found that only one in six savers intends to make a change to their plan investments and even fewer (13%) are likely to increase their contribution amount in the near future.

By adopting a data-driven approach that models the impact of plan design changes on income replacement scores, plan sponsors can begin to make design decisions that have measurable, positive outcomes for plan participants.

Putnam's PlanVisualizer tool for plan sponsors and advisors shines a light on retirement plan design and participant readiness — at all ages and salary levels.

Launch a demo

316229

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund’s bond investments are likely to fall if interest rates rise. Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions. You can lose money by investing in a mutual fund.

Putnam Retail Management.