Many taxpayers see the new year as a time to take a fresh look at financial plans.

The IRS recently announced the tax figures and contribution limits for 2022.

A first step for investors in tax planning for the year ahead is to determine their tax bracket. Putnam’s “2022 tax rates, schedules, and contribution limits” can be a useful reference to review with a financial advisor.

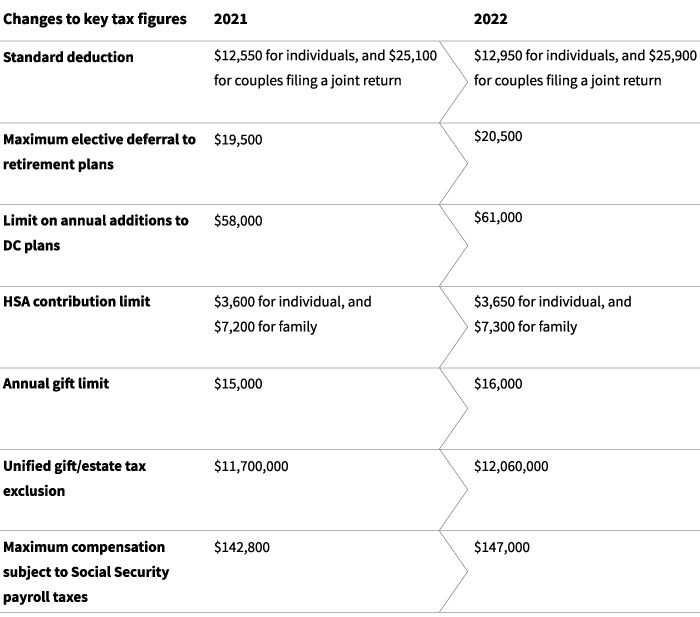

While most key tax figures had only slight changes for 2022 compared with 2021, there are areas where individuals may want to consider revisions to their tax strategy in the coming year. For example, the maximum amount a participant can defer salary into a defined contribution plan increases from $19,500 to $20,500.

Here’s a look at some of the key tax figure changes for 2022:

Additional tax changes possible

It’s also important to note that additional tax changes may be introduced this year. Talks in Congress to move the Build Back Better social spending legislation forward were stalled at year-end. However, Democratic leadership is planning to renew discussions to try to advance some of the key priorities of the bill. If there is an agreement, there may be tax-related changes as part of the overall package.

Whether or not some of these tax increases would take effect retroactively to the beginning of 2022, when legislation is passed, or next year, is unknown.

For example, two tax areas that could change are the Child Tax Credit (CTC) and the SALT (state and local tax) deduction.

Additionally, there may be modifications to retirement savings provisions later this year. The proposed SECURE 2.0 legislation would increase catch-up contributions to retirement plans for older participants and gradually raise the RMD age to 75. Read more about SECURE 2.0 in our blog.

Planning considerations

Even the slight changes set for 2022 can present opportunities for taxpayers to save or gift more. Here are some ideas to discuss with an advisor.

- Review retirement accounts / HSAs to increase contributions to the new maximum if possible

- Consider using the higher annual gifting limit to transfer wealth to other family members, including 529 plans that allow five years’ worth of gifts to be made up front

- For those with considerable assets, consider large gifts now based on the current lifetime gift/estate exclusion before the sunset provision takes effect at the end of 2025. At that time the lifetime amount is slated to be roughly cut in half

- Monitor developments on Capitol Hill to prepare for potential tax law changes as part of negotiations around the Build Back Better legislation. For example, if the SALT deduction limit is increased, discuss strategies with your advisor or tax preparer on how to best leverage the increase in the limit (such as bunching deductions if possible)

328153

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.