While filing for federal financial aid with the FAFSA form can seem daunting, it is critical when trying to access the different types of funds available for students planning to go to college.

Federal financial aid helps students by providing loans, grants, and work-study programs.

Families may want to maximize the opportunity for federal aid, especially since changes to the form are on the way this year that could impact the amount of aid awarded. FAFSA forms for the 2024–2025 academic year (which families would typically complete starting in October 2023) include some key changes that resulted from federal budget legislation signed into law late in 2020. See our post, “Changes on the horizon for FAFSA."

Importance of federal aid

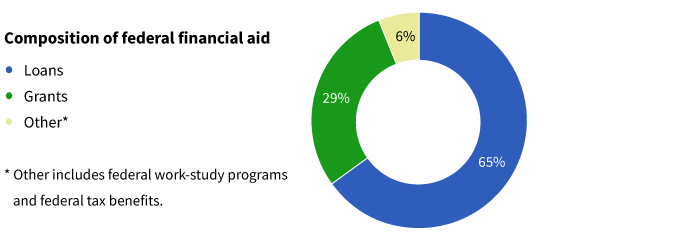

About $130 billion in total federal financial aid will be awarded this year. More than half of undergraduate students receive some type of aid, including federal student loans, according to the College Board (Trends in Student Aid 2023), with the average grant totaling about $10,500.

Source: College Board.

Simplified form may draw more applicants

The first change that applicants will see is a simplified form.

Even with the broad availability of federal aid, fewer families are applying. In fact, the number of families filing the FAFSA form dropped to 71% in 2022 from 85% in 2015, according to Sallie Mae (How America Pays for College 2023).

Sallie Mae also surveyed families that didn’t apply and found 30% of parents thought their income was too high to be eligible for aid. The second-most-cited reason (20%) was they “had problems with the application or found it too complicated.”

For the upcoming FAFSA form, applying to the 2024–2025 academic year, the questionnaire will be shortened and simplified. The Department of Education indicated the number of questions will be reduced to 36 from 100.

In addition, the form will be delayed from its typical release on October 1 to December 2023, due to the changes being enacted.

Three key changes to the FAFSA form this year

1. Treatment of grandparent-owned 529 accounts

As part of the FAFSA filing process, assets held by the parent or student (known as the “asset test”) and income reported by the parent or student (“income test”) are considered. In the past, 529 savings accounts owned by a non-parent (such as a grandparent) for the benefit of the student were not reported on the FAFSA form as part of the “asset” test. However, distributions from those accounts were generally considered income to the student and would be reported as such in the next FAFSA filing season, potentially causing a drastic reduction in aid awarded. In a positive development going forward, distributions from 529 accounts owned by non-parent family members will not be considered income to the student.

2. Households with multiple students in college at the same time

Historically, the calculation for federal financial aid has provided relief for families who have multiple students attending college at the same time. However, with the next FAFSA filing, this will no longer be the case. While lower-income households will not be affected due to how student aid is calculated, middle- and higher-income households could see a decrease in aid if there are multiple children in college at the same time.

3. Changes for divorced parents

For applications involving divorced parents, the new form will redefine “custodial parent.” Beginning with the next FAFSA filing, the calculation of aid will be based on income from the parent who provides the most financial support for the student, instead of the parent where the student lives most of the time. For FAFSA purposes, the definition of “custodial parent” will change to whoever provides the most financial support regardless of where the student lives (note that both parents will have to provide financial information).

Other modifications

Some of the changes in the 2020 legislation have already been implemented, including the shift from the Expected Family Contribution (EFC) to what is now called the Student Aid Index (SAI), the basis for calculating aid. The calculation is expected to expand access to the federal Pell Grant program to more students.

In tandem with the ease of applying to more colleges via the Common Application, the new FAFSA process will allow students to list as many as 20 colleges, up from the current total of 10. Lastly, there is an “income protection allowance” that is applied to parents and students. This allowance shelters a certain amount of income each year from being considered in the calculation. For the next FAFSA filing, these figures will be increased (20% higher for parents, 35% higher for students).

Tips for families seeking aid

- It is more favorable for assets reported on the FAFSA to be owned by the parent, rather than the student. The asset test considers a higher percentage of student-owned assets (such as a custodial UGMA or UTMA) than assets owned by parents. With the recent changes to the FAFSA, it may be more advantageous for non-parents, such as grandparents, to remain as an owner of a 529 account, instead of making contributions to a 529 account owned by a parent.

- It’s important to remember that the SAI considers income from the “prior prior” year tax return, referred to as the base year. This means the FAFSA application available in the fall of 2023 will consider the 2021 income tax return (generally filed by April of 2022). If receiving financial aid is a goal, you may want to avoid liquidating appreciated assets such as mutual funds that may result in large capital gains that increase adjusted gross income (AGI). This would have a negative effect on financial aid.

- Consider the tax implications of a Roth IRA conversion, which will increase AGI and may have an impact on aid eligibility. If possible, execute a Roth conversion before college and prior to the tax year that the financial aid application is based on. Also, consider paying the tax bill on the Roth conversion from other assets that may reduce total assets considered for the FAFSA asset test.

- Be aware that, in addition to the FAFSA, many families, especially those applying to private institutions, will have to complete the CSS Profile. This filing is used by colleges to determine their own institutional aid awards and will consider additional financial information that the FAFSA does not include. For example, a CSS may consider home equity, business-related income, and savings held in non-parent-owned college savings accounts such as 529s. In addition, the CSS Profile will ask for information about medical expenses that may hinder a family’s ability to pay for college.

Craft a plan for college

Considering the cost of higher education, parents and students should look to consider all sources available to fund college including financial aid, 529 savings accounts, scholarships, tax benefits, employment income, etc. For more help, explore our additional resources such as “Early college planning for a growing family” and “Four-year action plan.”

334271

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.