The COVID-19 pandemic is taking a broad economic toll— from layoffs, to business closings, to reduced hours and earnings. It may also have consequences for Social Security benefits.

Lower earnings and Social Security

Earning less in 2020 could have a slight impact on the future retirement benefits of some workers. The calculation for Social Security retirement benefits is based on your average indexed monthly earnings (AIME).

- In applying a worker’s AIME to determine a Primary Insurance Amount (PIA), the highest 35 years of a worker’s earnings history are considered. (The PIA is the actual benefit the worker is entitled to at his/her full retirement age)

- Before the pandemic, 2020 might have been one of those top 35 (indexed) earning years for some workers

- While this may not be a significant factor in future benefits, it may be something that future retirees will want to understand

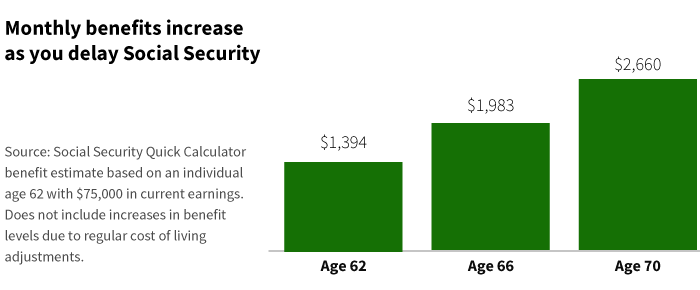

Filing for Social Security benefits earlier than expected

Some workers may have been forced to retire earlier because of COVID-19 and to file for Social Security retirement benefits sooner than planned.

The April jobs report revealed that the unemployment rate among older workers — age 65 and older — reached 15.6%, which was the highest level since the government began tracking the data in 1948 (Urban Institute).

More than half of older unemployed workers are at risk of being forced into early retirement, according to the Schwartz Center for Economic Policy Analysis. SCEPA’s research noted that the total number of unemployed workers retiring earlier than planned could reach four million this year.

Individuals turning 60 this year could take the biggest hit

Individuals turning age 60 in 2020 may experience the biggest impact on future benefits. In addition to the top 35 working years, the Social Security calculation includes an overall indexing of wages based on national statistics. This number, the national Average Wage Index (AWI), is used to apply an inflation factor against prior earnings.

Wage indexing depends on the year in which a person is first eligible to receive benefits. For retirement, eligibility begins at age 62. According to the Social Security Administration, if a person reaches age 62 in 2020, then this is their year of eligibility. An individual’s earnings are always indexed to the average wage level two years prior to the year of first eligibility.

Because of the economic impact of the pandemic, the national average of worker earnings in 2020 may be reduced by somewhere between 5% to 10%. For workers turning age 60 this year, their indexing factor will be based on 2020 data which will, in effect, lower their retirement benefit. The higher the index figure when you turn 60, the better result for your retirement benefit calculation. The lower the index figure, the worse result.

Unless Congress addresses this issue, these affected workers may see an annual decrease in their benefit of roughly $1,500 over (potentially) several decades of retirement. (Center for American Progress, July 2020). This represents a significant loss of benefits for these individuals.

Social Security solvency under threat

In recent House testimony, Social Security actuarial research indicated that reduced earnings and less payroll tax revenue, could accelerate the program’s insolvency. If earnings were reduced in 2020 by 15%, the Social Security trust funds could be depleted in middle of 2034, earlier than the current projection of 2035. If earnings are reduced for two years, trust funds could be depleted by late 2033 or early 2034.

Nearly 90% of retirees receive Social Security benefits. On average, Social Security benefits represent about 33% of income for seniors. Considering that most investors include these benefits in retirement plans, it is important to understand the impact of the economic challenges this year. Consult a financial professional who is monitoring these issues and possible policy changes to Social Security.

323035

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.