Last year’s economic slowdown caused added financial stress for many families.

As students and families look ahead to college, the cost may seem daunting. Some families may not fully understand the price of tuition and fees, leading them to underestimate or overestimate what will be needed. And students may be reconsidering their goal of higher education because they believe it’s too expensive.

There are many resources online to research tuition, fees, and room and board. By creating a college savings strategy, with guidance from a financial advisor, families can use a variety of ways to meet costs and help students achieve their goals.

Heightened focus on finances

Several surveys conducted this year found that many families are unsure about the cost of college. In the Princeton Review’s “2021 College Hopes and Worries,” 63% of the more than 14,000 college applicants and parents surveyed estimated their college costs would be more than $75,000. Of those, 37% said they expected the price tag to be more than $100,000.

A separate survey by ECMC, a nonprofit that helps student borrowers, found that fewer students are planning to go to college because they believe it costs too much. The spring survey of high school students found that the likelihood of going to college fell to 53% from 71% in the past eight months.

Research the cost

The College Board publishes average costs and trends in financial aid for public and private colleges and universities each year. Average tuition, fees, and room and board for the 2020-21 academic year increased by 1% to $22,180 for in-state students at four-year public colleges, according to the College Board. The same expenses at four-year private institutions rose by nearly 2% to $50,770. In recent years, college cost inflation has trended down — a win for families and students. Many remember the not-so-distant past, when college inflation increased much more dramatically and generally higher than core inflation.

The College Board’s BigFuture site offers online tools and calculators to aid in the savings process. BigFuture encourages families to focus on net price – what you actually pay – versus published sticker price.

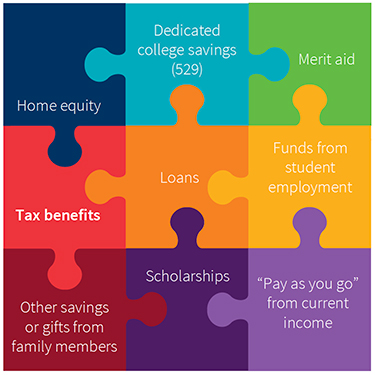

How do families pay for college?

Most families rely on a combination of resources to pay for college, according to Sallie Mae. These include income and savings, scholarships and grants, and student loans. The majority of families use the parents’ income as a significant source. In the 2018-2020 academic year, 85% of families used parent income and savings and contributed $13,721 on average.

Similar to the previous year, 37% of families used a college savings plan, such as a 529, to cover the cost of college.

As a share of college costs, parent income and savings made up 45% of the total, Sallie Mae found. Scholarships and grants covered 25% of costs. The remaining sources were student borrowing (11%), parent borrowing (9%), student income and savings (8%), and funds from relatives and friends (2%).

Advantages of a 529 college savings plan

Having an overall financial strategy is important as families strive to keep savings on track.

The 529 college savings plan remains a popular part of a savings strategy. One reason is the tax advantage.

- There are no federal income taxes on earnings while the account is invested. You pay no federal income taxes when the money is withdrawn to pay for qualified college expenses.

- Proceeds from a 529 savings plan account can be used at any accredited college to pay for tuition, fees, room and board, books, and other qualified expenses. In addition, up to $10,000 per student per year may also be used to pay tuition at any public, private, or religious elementary or secondary school.

- A special gift-tax exclusion allows five years' worth of gifts to a single beneficiary in a single year without triggering the federal gift tax.

- In certain cases, contributions to the account can be removed from an estate for tax purposes, yet account owners retain control over the assets. This benefit is unique to 529 plans.

Plan early

Early planning is helpful for families to reach education savings goals. Use our Four-year action plan to help stay on track for college planning throughout the high school years. For younger families, refer to our brochure: Early college planning for a growing family.

327079

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.