Effective this year, the IRS provides new life expectancy tables to calculate required minimum distributions from retirement accounts.

The new tables impact retirees as well as certain beneficiaries with inherited retirement accounts

The updated data reflects the fact that people are living longer. The resulting calculations mean that retirees may keep larger amounts of assets in their retirement plans.

Required distributions for beneficiaries

Certain account beneficiaries are also impacted by the new tables.

The SECURE Act requires many beneficiaries to distribute retirement funds by the end of the 10th year following the account owner’s death. However, some beneficiaries are still able to calculate RMDs based on their remaining life expectancy. These include spouses, eligible designated beneficiaries (EDBs), and those who inherited an account from an owner who died prior to 2020.

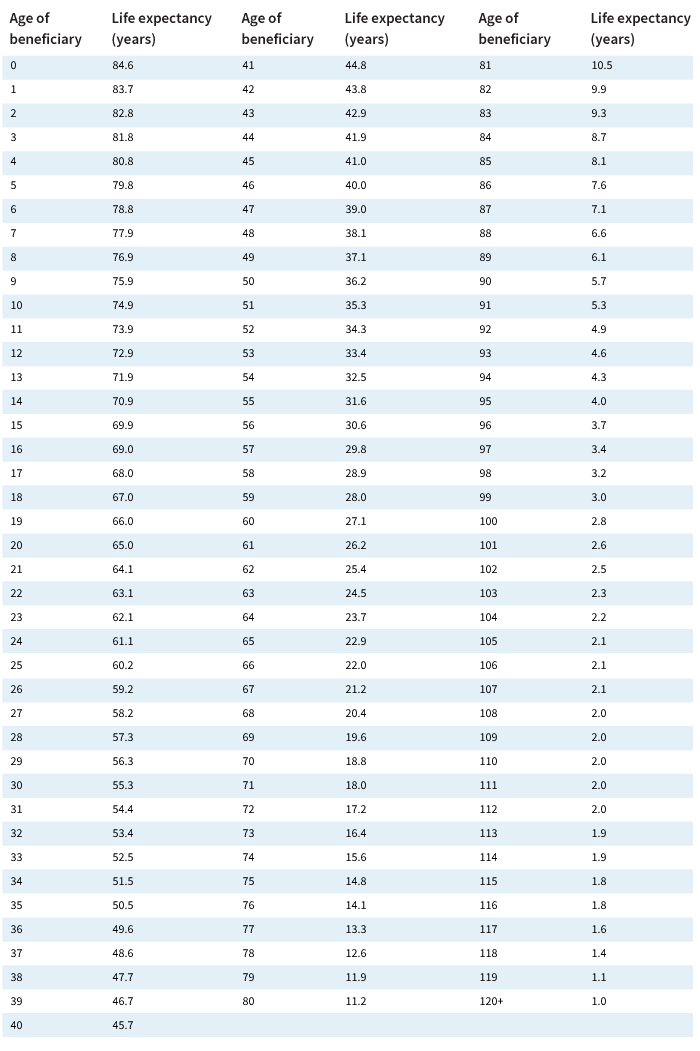

Required distributions for eligible account beneficiaries are calculated using IRS single life expectancy tables. The beneficiary uses the table to determine a life expectancy factor based on their age as of 12/31 in the year after the account owner’s death. For each subsequent year, the RMD is calculated by applying the life expectancy factor reduced by one year. For example, the life expectancy factor for a 50 year-old beneficiary is 36.2. The first distribution for the beneficiary would be based on that figure (36.2), while the distribution for the following year would be based on a life expectancy factor of 35.2 and so on.

Single life expectancy table

*As of 12/31 of the given year.

Source: Treasury Regs. Sec. 1.401(a)(9)-9.

How are RMDs calculated?

Beneficiaries of retirement accounts must generally use the single life expectancy table, which will result in a higher distribution amount than the uniform table.

Special transition rule to the new single life table

For beneficiaries who are already taking distributions based on their remaining life expectancy there is a rule that allows them to transition from the previous single life expectancy table to the new table. This will result in lower required distributions going forward. Here is an example of how this transition rule would apply.

- John inherited a large IRA from his father, who passed away in 2016, prior to the SECURE Act’s new 10-year rule

- Based on the single life table at that time, the life expectancy factor he used for his initial RMD in 2017 was 29.6 based on his age of 55, resulting in an RMD of $16,891 assuming an IRA value of $500,000 ($500,000 divided by 29.6 equals $16,891)

- For each subsequent year, John’s life expectancy factor is reduced by one (i.e., for 2018, the life expectancy factor is 28.6; for 2019, it’s 27.6; for 2020, it’s 26.6; and so on)

- Assume that, even after several years of distributions, the IRA value has grown to $600,000

- For 2022, his life expectancy factor for the RMD was slated to be 24.6, yielding an RMD of $24,390

- However, now that the IRS life expectancy tables have been updated, John can benefit from a transition rule to the new tables that will result in a lower RMD for 2022 and future years

- Under this transition rule, John refers to the life expectancy factor on the new single life table based on his age when he first started taking distributions (age 55)

- From the new table, for age 55, the life expectancy factor is 31.6

- To determine the factor for 2022, John must subtract 5 from 31.6 — one for each of the five years that have passed since he was age 55

- For 2022, his new life expectancy factor is 26.6 resulting in an RMD this year of $22,556, roughly $1,800 less than under the old table

Expert advice is important

It is important for individuals taking distributions on inherited accounts to be aware of the new rules so they’re not taking out more money than required, which may result in a higher tax bill. The rules can be complex, and individuals with inherited accounts may want to consult with a professional advisor.

328867

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.