In a move that may help retirees keep more of their savings longer, the Treasury Department recently updated the life expectancy projections used to calculate required minimum distributions from retirement accounts.

The new life expectancy tables, which become effective starting this year, were modified to reflect that Americans are living longer. In addition to retirement account owners, these changes will apply to certain beneficiaries with inherited accounts.

The new calculations will reduce RMDs and allow investors to retain larger amounts of assets in their retirement plans to account for the possibility they may live longer. The modification may also help retirees save on taxes due from required retirement distributions.

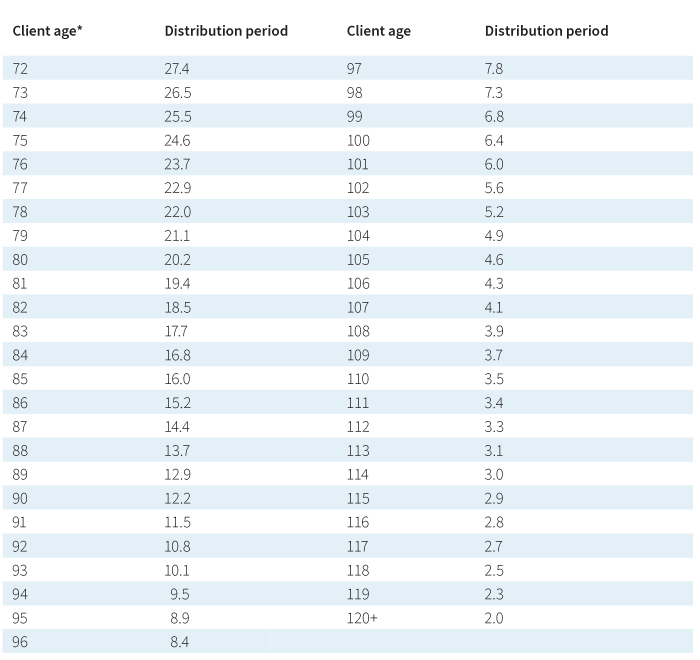

Uniform lifetime table

*As of 12/31 of the given year.

Source: Treasury Regs. Sec. 1.401(a)(9)-9.

RMD rules

For retirement account owners, the first RMD must be withdrawn by April 1 following the year you reach age 72. This is referred to as the required beginning date (RBD). Note that if you delay your first RMD to April 1, you will need to take another RMD by the end of that calendar year. This may have negative tax implications since you’re taking two distributions within one calendar year. Subsequent RMDs are due every year by December 31. There are exceptions to the age 72 rule if you’re still employed, participate in your current employer’s plan, and meet certain requirements such as not owning 5% or more of the company. The exception only applies to your current workplace plan, not any IRAs you may hold.

Harsh penalties apply for failing to take an RMD. The IRS imposes a 50% penalty of the amount that should have been withdrawn.

How does the RMD “math” work?

- The calculation for account owners is based on the IRS Uniform Life Expectancy Table.

- There is an exception for account owners whose spouse is the sole beneficiary and is more than 10 years younger. In this case, a different life expectancy table applies (Joint Life and Last Survivor Expectancy Table). This calculation will result in a lower RMD.

- Beneficiaries of retirement accounts (who are eligible for lifetime income distributions) must generally use the Single Life expectancy table, which will result in a higher distribution amount than the Uniform Table.

What is changing

Retirees would be required to withdraw less from their accounts. The changes also apply to beneficiaries, who would be required to withdraw less under the new lifetime expectancy guidelines.

Strategies for those who don't need RMDs for income

There are strategies that investors may consider if they do not rely on their RMDs for income in retirement for daily expenses.

- Use RMDs to fund a 529 college savings plan. Grandparents and other family members who do not rely on RMDs may prefer to use these funds to help fund a college education. The RMDs will generally have to be reported on a tax filing as income. Once invested in a 529 savings plan, the funds can grow and be distributed free of taxes if used for qualified education expenses.

- Donate IRA assets to a charity. This IRA provision allows retirees age 70½ and older to donate up to $100,000 tax free from their IRA each year, including required distributions.

Review with an advisor

The IRS requires RMDs to ensure that individuals do not defer paying taxes on retirement savings indefinitely. If you own a traditional IRA, age 72 is an important milestone. It’s important to understand the rules around RMDs and discuss the schedule with your financial advisor. In addition, there are separate rules for beneficiaries who inherit IRAs and other retirement accounts.

For more details on RMDs, see Putnam’s investor education piece, “What you need to know about required IRA withdrawals.”

328317

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.