As year-end approaches, taxpayers should get a sense of their projected income for this year to determine their marginal income tax bracket. This estimate can provide clarity on two questions:

- What is the cost of adding more income before the end of the year? (Or, conversely, what are the savings for reducing income before the end of the year?)

- How much income can I realize before creeping into the next tax bracket?

These are basic questions to answer when looking at potential transactions before year-end, including Roth conversions, charitable contributions, and harvesting tax losses. Another factor for taxpayers to consider is while current tax rates are historically low, they are scheduled to expire at the end of 2025.

There are several strategies that investors may consider to make the most of their tax brackets.

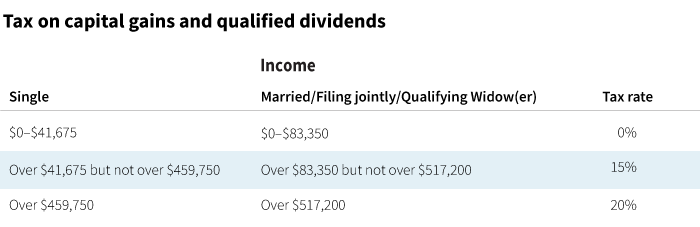

Don’t forget about the 0% tax rate on capital gains and dividends

Taxpayers in lower income tax brackets may be able to avoid taxation on long-term capital gains and qualified dividends. Here are the current tax rates and income thresholds for 2022

Additional 3.8% federal net investment income (NII) tax applies to individuals on the lesser of NII or modified AGI in excess of $200,000 (single) or $250,000 (married/filing jointly and qualifying widow(er)s). Also applies to any trust or estate on the lesser of undistributed NII or AGI in excess of the dollar amount at which the estate/trust pays income taxes at the highest rate ($13,450).

For example, consider a married couple, age 65+, filing a joint tax return and claiming the standard deduction of $28,700.

- Assume their income is $80,000 before deductions

- Taxable income would be $80,000 less the standard deduction of $28,700 = $51,300

- The couple could realize about $30,000 of long-term capital gains and/or qualified dividends at a zero percent tax rate (the threshold for 2022 is $83,550)

With the risk of tax rates edging higher in the future, some investors may want to consider “filling up” their tax bracket with additional income. A tax professional can help determine whether adding more income before year-end makes sense.

Maximize the tax bracket potential

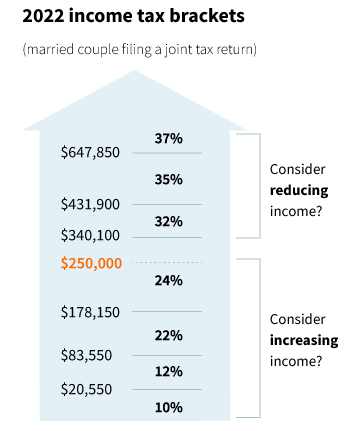

Taxpayers may use a Roth IRA conversion to fill the remaining room in a tax bracket with additional income. For example, an individual taxpayer with projected taxable income in 2022 of $150,000 could conceivably convert roughly $20,000 of a traditional IRA to a Roth and still be subject to the 24% marginal tax bracket. Any additional income would be taxed at the much higher 32% marginal tax bracket. These funds (and subsequent appreciation) could be withdrawn tax free in the future, assuming conditions are met.

For the full list of all brackets and other tax information, see "2022 Tax rates, schedules, and contribution limits."

Target a threshold

If taxpayers filing a joint return are realizing long-term capital gains or qualified dividends, it may make sense to not exceed $250,000 in income (defined as modified adjusted gross income). By staying under the $250,000 threshold, taxpayers may avoid the 3.8% surtax on investment income. For individuals, the threshold for the 3.8% surtax is $200,000.

Is it wise to reduce income?

Taxpayers in higher income tax brackets may benefit from reducing taxable income before the end of the year. Some ideas include the tactical use of deductions such as charitable giving or retirement account contributions.

Tax planning is specific for individuals

Knowing the expected tax bracket is a good start for year-end planning. Investors should discuss the implications of tax mitigation strategies with a financial advisor who understands their individual tax situations. Implementing these strategies before year-end may help optimize the advantages of the current tax brackets.

331624

For informational purposes only. Not an investment recommendation.

This information is not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Putnam does not provide tax or legal advice.